- Vietnam’s rise can pull assembly orders away from China, especially under tariff pressure.

- Chinese suppliers with only low-cost capacity face greater hollowing-out risk.

- Companies with engineering, supply-chain depth and customer control are harder to replace.

Offshore Transfer to Southeast Asia: A Long-standing Issue

Since the beginning of Trump's presidency, the topic of industrial transfer to Southeast Asia has become a hot one. When tariffs were increased, several leading companies in the industry immediately requested their suppliers to establish factories in Southeast Asia, which was quite uncomfortable for these industry leaders. Continuous visits to Southeast Asia, renting factory spaces, and setting up plants followed.

#### Case Study: Stanley Black & Decker

By late 2020, industry giant Stanley Black & Decker closed its factory in Shenzhen and transferred some of its production capacity to Suzhou, while another portion was moved to Mexico. The transfer to Suzhou was driven by the city's overall high efficiency, which has been a model factory for Stanley Black & Decker globally for many years. Additionally, the land in Suzhou is owned by the company itself, eliminating rental costs. The move to Mexico was primarily aimed at reducing the financial and risk impacts of trade frictions between China and the United States.

Another major player, Dandong TTI (Tronxy), began its strategic shift to Vietnam in 2019. On one hand, this move was aimed at avoiding risks associated with trade frictions. On the other hand, it is rumored that the local government offered extremely favorable tax and land conditions, which could offset any losses from the transition. Additionally, TTI has a long-term optimistic outlook on Vietnam's development, seeing an opportunity to replicate its rapid growth phase in China during the 1990s when it first established factories there.

With the actions of these industry leaders, many are once again questioning whether the entire sector will be moved to Southeast Asia, leading to industrial hollowing out.

Firstly, we need to clarify that Stanley Black & Decker and TTI primarily operate in North America. All their current moves are aimed at responding to tariffs in the North American market. In the short term, customers outside North America generally will not ask suppliers to move to Southeast Asia, because doing so would only increase costs.

Only Shark and Bissell require suppliers to move to Southeast Asia, with their corresponding suppliers being Kingclean, Chun Guang Technology, Aiper Intelligent, Fugia, Xinbao, etc. For 95% of the factories in this industry, there will be no impact.

Take Vietnam as an example; currently, the overall manufacturing cost in Vietnam is slightly higher than in China, and its efficiency is also lower than that of China. After factoring in tariff costs, exporting from Vietnam becomes more economical.

What if the manufacturing costs in Vietnam and China become the same in the future?

Analysis of the Future Landscape for Cleaning Appliances in the Context of Ongoing Sino-U.S. Trade Frictions

Firstly, we assume that Sino-U.S. trade frictions will continue over the next few years, and relations with other countries will remain similar to their current state.

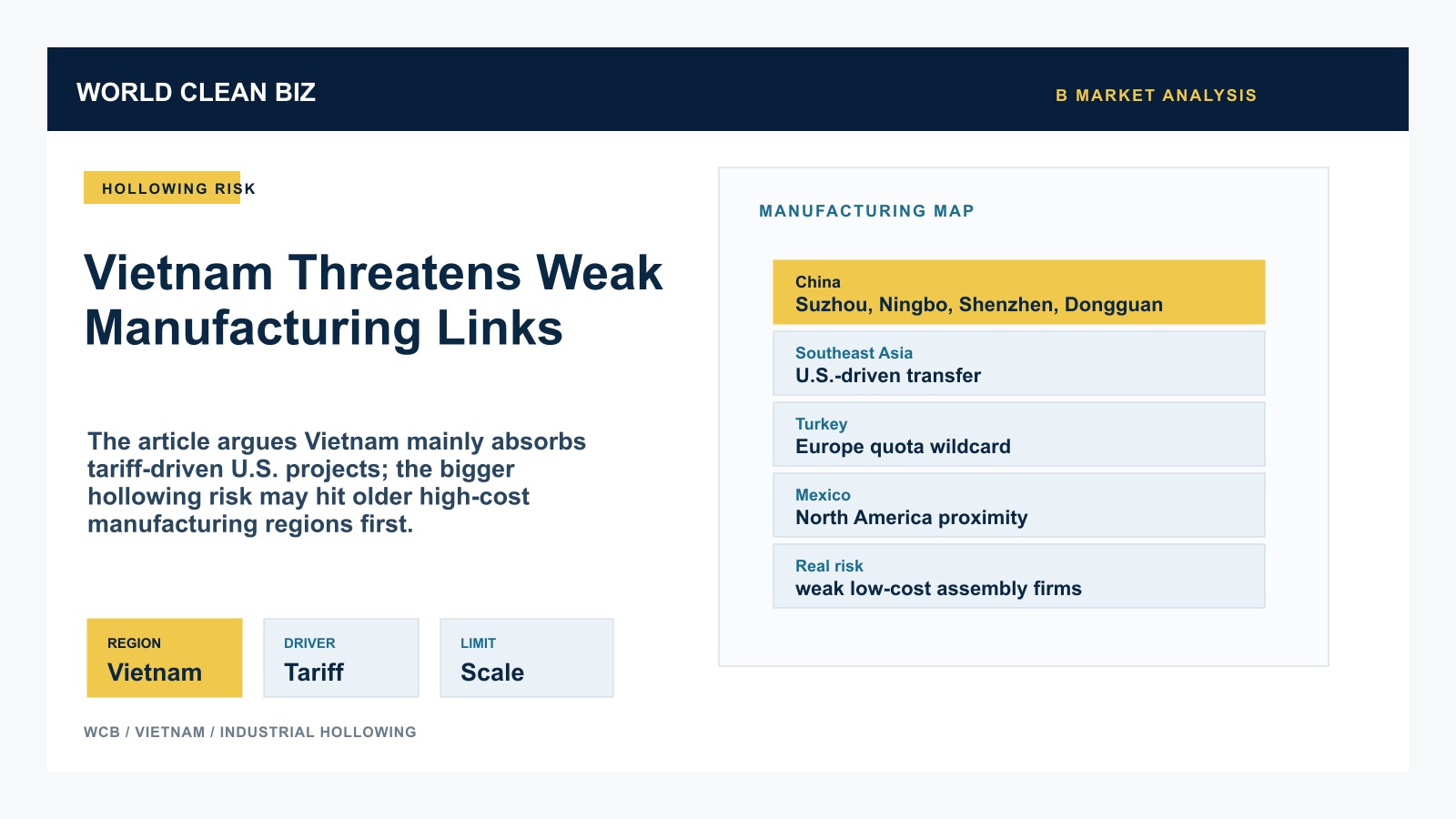

Major Manufacturing Countries in the Cleaning Appliances Industry

- China. Currently, major manufacturing centers are located in Suzhou, Ningbo, Shenzhen, and Dongguan. From recent developments, the importance and production capacity of Suzhou (vacuum cleaners, hard floor washers) and Shenzhen (robot vacuums) will continue to strengthen.

- Southeast Asia. As the largest beneficiary of Sino-U.S. trade frictions, Southeast Asian countries have recently taken on a large number of projects from North American clients. Currently, major manufacturing hubs include Vietnam, Indonesia, and Malaysia. Malaysia primarily hosts factories for Dyson-related products, including later transfers by Bissell to companies like VS. Meanwhile, LG and Samsung, South Korean brands, mainly establish their bases in Vietnam, with the leading Chinese manufacturers also focusing on Vietnam.

From a competitive standpoint, Vietnam stands out as the most competitive country in Southeast Asia due to its rapid growth over recent years. In the future, Vietnam will continue to pose some threat to China. However, given the limited population and resources available for taking on transferred projects. Vietnam will mainly take on relocation projects from several brand customers serving the U.S. market.

- Turkey. Turkey has been increasing tariffs on cleaning appliances in recent years to achieve localized manufacturing. Given its proximity to Europe, if Europe imposes quotas on Chinese products, the Turkish market could potentially take advantage of transshipment trade to capture a portion of China's market share, similar to how Turkish brands like Beko and Arcelik have become major players in European television production due to quota restrictions.

If Europe implements quotas for cleaning appliances, Turkey might rise as a significant player.

- Eastern Europe. Previously, Western European brands such as Electrolux had manufacturing bases in Eastern Europe. The advantage of Eastern Europe is its proximity to the market and low transportation costs. However, China's complete industrial chain and lower production costs have led to the closure of several Eastern European bases over the past two years, with orders shifting to domestic companies. Overall, Eastern Europe appears to lack significant manufacturing advantages.

- Mexico. Due to its proximity to the U.S. market and preferential policies under the U.S.-Mexico-Canada Agreement (USMCA), products shipped through Mexico to the U.S. have very low tariff costs. This is why major companies like Black & Decker establish their factories in Mexico, primarily serving North American clients.

Apart from North American markets, Mexico offers no significant advantages.

- Taiwan and South Korea. Taiwan and South Korea still maintain some small-scale manufacturing enterprises, with local whole-machine manufacturers focusing on the high-end "local production" market. Additionally, parts suppliers for major brands like Samsung and LG operate around their Vietnam factories, such as numerous Korean suppliers in the vicinity of these plants.

From the perspective of these manufacturing bases, if policy factors are excluded, only Southeast Asia poses a real threat to China's supply costs and efficiency. If Southeast Asian manufacturing becomes more prominent, it will primarily impact European and South Korean-Taiwanese small-scale manufacturers rather than Chinese manufacturers.

Some friends have informed me that when they visit Vietnam to find suppliers, the most expensive ones are from South Korea and Taiwan due to the poor quality of local Vietnamese suppliers who rely on these large enterprises. Once local Vietnamese suppliers grow stronger, the biggest impact will be on these companies.

In the cleaning appliances sector, the only factor that can affect Chinese manufacturers is tariff and quota policies in various countries. Even if some countries implement policies against China, their actual impact on China's industrial chain is limited.

The rise of regions like Vietnam and Turkey may have a limited impact on China but could significantly affect original developed countries such as South Korea, Japan, and Europe, potentially rendering them completely uncompetitive.

The rise of these countries might be the final blow to the hollowing out of developed nations' industries.