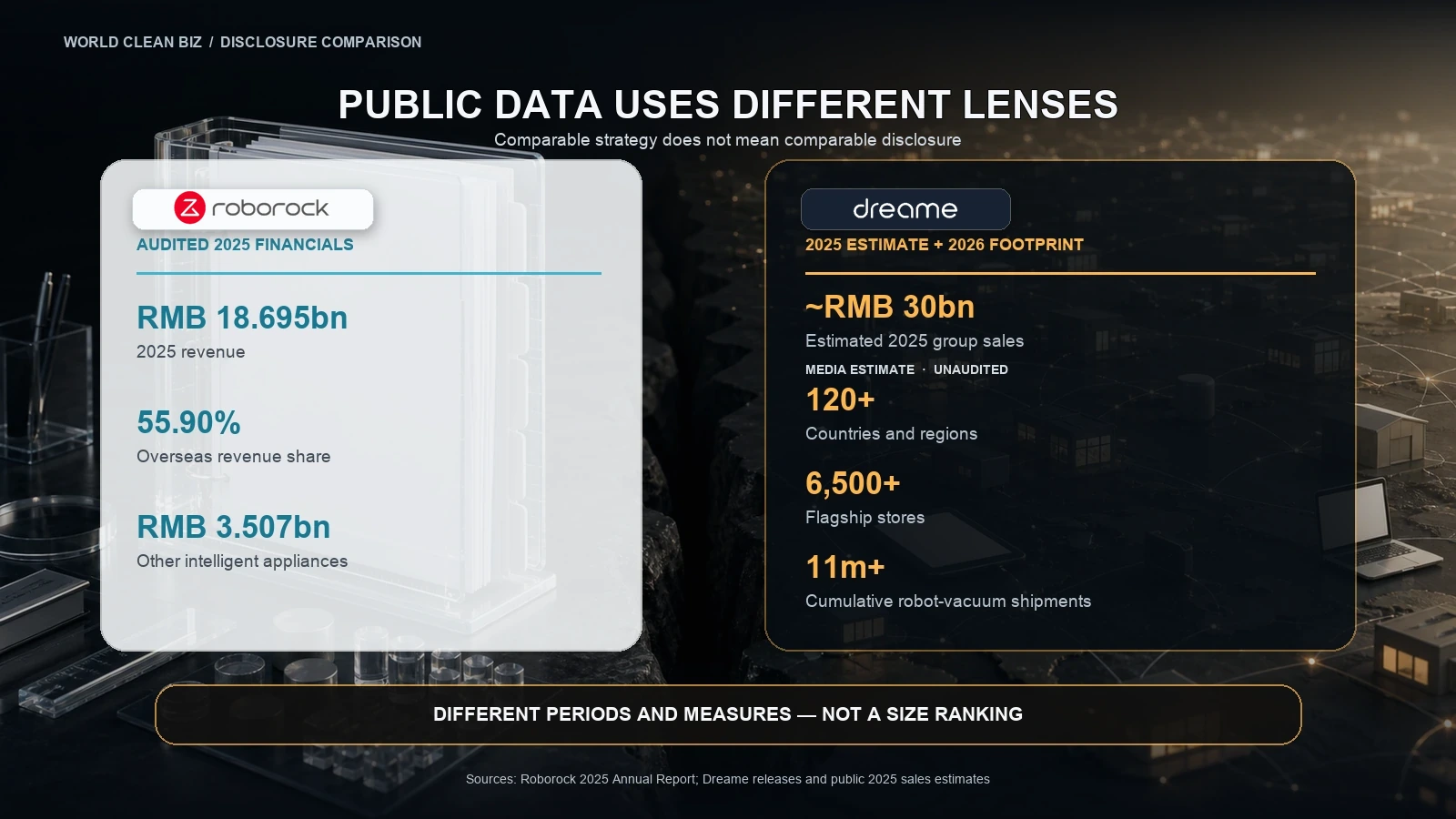

- Roborock reported RMB18.695 billion in audited 2025 revenue while expanding into adjacent home-maintenance categories.

- Public estimates put Dreame's 2025 group sales at about RMB30 billion, but the private company does not publish comparable audited financial statements.

- For suppliers, retailers and distributors, disclosure quality, channel economics and service capacity matter more than a model-by-model specification contest.

Search for “Roborock vs Dreame” and most comparisons quickly turn into a contest over suction figures, mop designs, obstacle avoidance and app features. That is useful if the only question is which robot vacuum to buy.

For the cleaning industry, the more important comparison is no longer between two machines. It is between two companies that started from a similar Chinese technology and supply-chain environment but are now building very different growth systems.

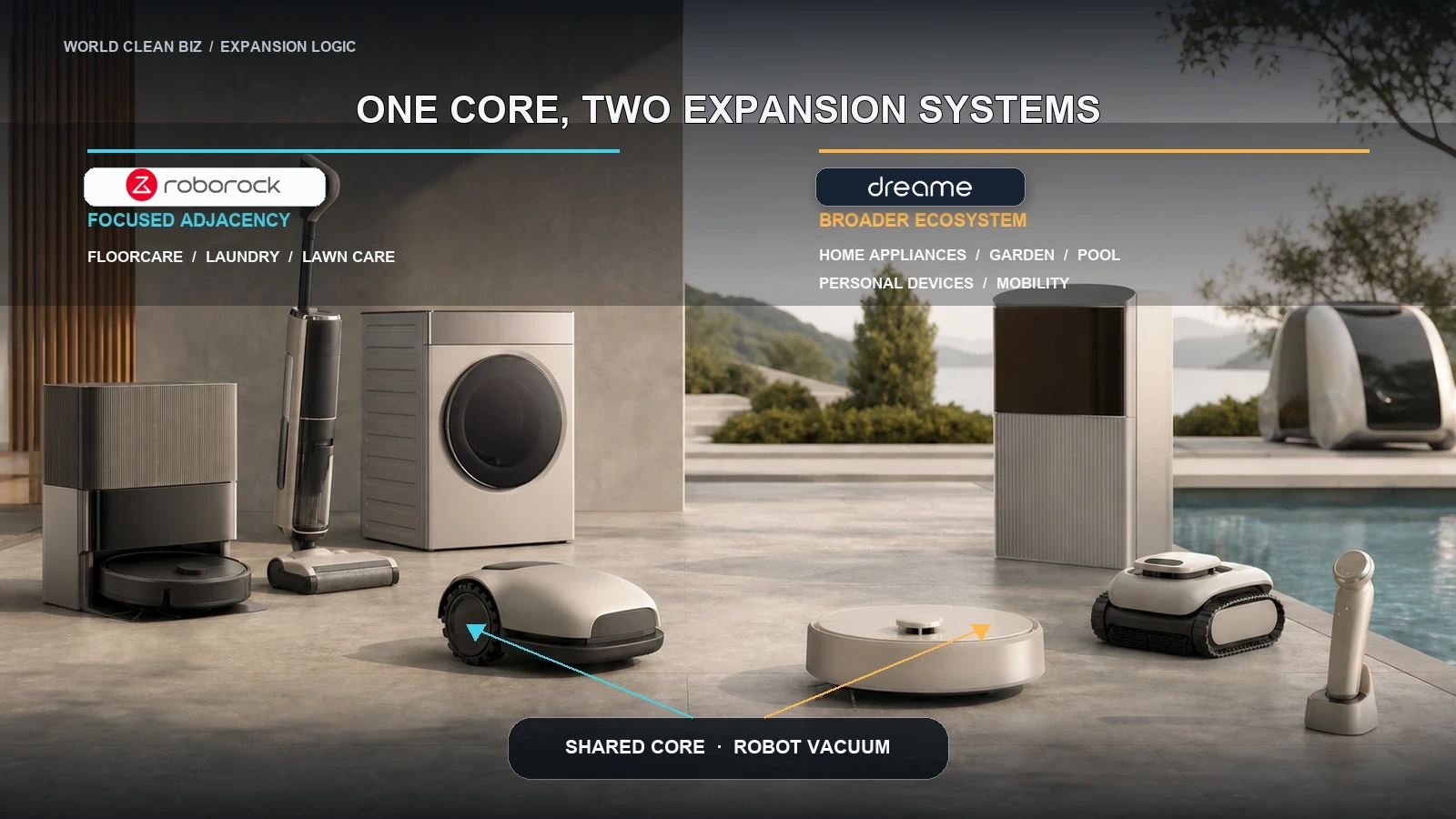

Roborock is still anchored to robot vacuums, but it is expanding into adjacent categories under the financial discipline of a listed company. Dreame is using cleaning technology as the starting point for a much broader platform spanning the home, garden, pool, personal care and even smart mobility.

The real Roborock vs Dreame question is therefore not which brand has the stronger specification sheet. It is which model of expansion can remain coherent when product portfolios, channels, inventories and after-sales obligations all become larger.

Roborock vs Dreame at a Glance

| Dimension | Roborock | Dreame |

|---|---|---|

| Historical core | Robot vacuums and floorcare | High-speed motors and intelligent cleaning appliances |

| Current strategic anchor | Global robot-vacuum leadership with adjacent category expansion | A multi-category smart-living and robotics ecosystem |

| Expansion pattern | Wet-dry floorcare, laundry and robotic lawn care around the home-maintenance market | Cleaning, major appliances, personal care, lawn care, pool care and smart mobility |

| Disclosure model | Public company with audited revenue, profit, margin and cash-flow data | Private company; estimated 2025 group sales of about RMB30 billion, but no comparable audited annual report |

| Main organizational advantage | A visible operating model and a strong global robot-vacuum base | Product speed, broad engineering ambition and aggressive category creation |

| Main strategic risk | Margin pressure and the difficulty of building meaningful second growth curves | Portfolio complexity, channel inventory, service requirements and a diluted brand proposition |

This distinction needs one qualification. Describing Roborock as “focused” no longer means it is a single-category company. Its latest financial disclosure shows that diversification is already material. The difference is the distance each company is willing to travel from its original category.

A Similar Xiaomi-Ecosystem Beginning, but Not the Same Company

Both brands are often described loosely as “Xiaomi companies.” That description is convenient, but it is no longer an accurate way to understand either business.

Roborock says it was established in July 2014, received investment from Xiaomi that September and became a member of the Xiaomi ecosystem. Its first major product was the Mi Home robot vacuum. Roborock later developed its own brand, distribution system and product identity, and listed on Shanghai’s STAR Market in 2020. It is an independently operated public company, not simply a Xiaomi product line. Its current shareholder disclosures still include a Xiaomi-related investment entity, but that is different from saying Xiaomi owns the business.

Dreame’s own history pages require more care. One official page traces the company to 2015, while another describes 2015 as the beginning of the founding team’s high-speed motor work and 2017 as the formal establishment of Dreame Technology. The company says it joined the Xiaomi ecosystem at the end of 2017. Dreame subsequently built its own brand across cordless vacuums, robot vacuums, wet-dry cleaners and personal care.

The Xiaomi ecosystem mattered to both companies because it offered early product opportunities, supply-chain connections and market validation. But their current competition is not an internal Xiaomi contest. It is a contest between two independent brands trying to turn Chinese engineering and manufacturing capabilities into global brand power.

Roborock’s Route: Expand from a Proven Global Core

Roborock’s strongest argument is not that it has avoided expansion. It is that the company is expanding from a core business whose economics can be seen.

According to Roborock’s 2025 annual report, revenue reached RMB18.695 billion, up 56.51% year on year. Revenue from robot vacuums and related accessories was RMB15.173 billion, still more than four-fifths of the company’s total revenue. This remains a robot-vacuum-led business.

At the same time, revenue from other intelligent appliances reached RMB3.507 billion, up 227.75%. The company introduced wet-dry floor cleaners, washer-dryers and robotic lawn mowers alongside its established robot-vacuum portfolio. Roborock has therefore moved beyond the simple “one company, one category” description.

The important point is how this diversification appears in the accounts. Growth came with pressure. Gross margin in the main business declined, sales expenses rose to RMB4.894 billion, and net profit attributable to shareholders fell 31.03% to RMB1.363 billion. Overseas main-business revenue reached RMB10.442 billion, or 55.90% of the total, but global expansion, self-operated channels, tariff exposure, marketing and a wider product mix all carried costs.

Roborock’s 2026 first-quarter report continued the same picture. Revenue grew 23.31% to RMB4.227 billion and reported net profit increased 20.83%, while operating cash flow was negative RMB394 million and inventory rose from the end of 2025. The company attributed the cash-flow change partly to timing in its resale production model, but the figures still show why rapid global growth must be judged through more than revenue.

This is Roborock’s strategic discipline and its strategic burden. Every new category has to survive public scrutiny. Investors can see whether a second curve is adding revenue, lowering margin, consuming cash or increasing inventory.

That does not make Roborock conservative. Its 2025 disclosure included robotic lawn mowers, washer-dryers and more experimental robotic structures. It means the company’s expansion is continually pulled back toward measurable operating results.

Dreame’s Route: Turn Cleaning Technology into a Platform

Dreame presents a different idea of what a cleaning technology company can become.

The company’s established base includes robot vacuums, cordless vacuums, wet-dry floor cleaners and high-speed hair dryers. These categories share parts of an engineering foundation: high-speed motors, airflow, sensing, SLAM, batteries, mechanical design and increasingly automated base stations.

By 2026, however, Dreame’s public ambition had moved well beyond a cleaning portfolio. At CES 2026, the company described an AI-powered whole-home ecosystem covering smart cleaning, kitchen appliances, environmental appliances, personal care, lawn care and pool cleaning. Its product display included the X60 Max Ultra Complete robot vacuum, A3 AWD Pro robotic lawn mower and Zircon 2 Ultra robotic pool cleaner.

The Dreame NEXT 2026 event pushed the message further. Dreame grouped products under smart home, outdoor care, personal devices, personal care and smart mobility. The company’s argument is that motors, algorithms, perception and robotic structures can be reused across many categories, turning individual product features into a wider engineering platform.

That is a much more expansive thesis than selling more types of floorcare appliances.

Dreame also says its robot-vacuum business has gained substantial global scale. In a June 2026 announcement, the company said, citing IDC, that Dreame ranked first globally in robot-vacuum unit sales and revenue in the first quarter of 2026. The same release said the business covered more than 120 countries and regions, had more than 6,500 flagship stores and had shipped more than 11 million robot vacuums cumulatively.

Public media estimates put Dreame’s 2025 group sales at approximately RMB30 billion. That estimate is useful as a broad scale signal, but it is not an audited figure and does not reveal the group’s product mix, margins, inventory, cash flow or the contribution of individual business units.

These are meaningful signals, but they are not equivalent to a public annual report. The IDC ranking is being relayed through a Dreame press release, and the company does not publish audited segment revenue, gross margin, inventory or cash-flow data comparable with Roborock’s disclosures.

Dreame’s strategic attraction is easy to see: if its underlying technologies can migrate across categories, the company can keep opening new markets rather than depend on one maturing product. Its strategic risk is equally clear: a technology that transfers in the laboratory does not automatically transfer through retail, installation, repair and long-term service.

Two Types of Diversification

The Roborock vs Dreame comparison becomes more useful when both companies are recognized as diversifying businesses.

Roborock’s new categories remain relatively close to home cleaning and maintenance. Wet-dry floor cleaners extend the company’s floorcare position. Washer-dryers move into another household cleaning task. Robotic lawn mowers take mapping, navigation and autonomous movement outdoors. These moves are significant, but the commercial logic remains adjacent to the original brand promise: automate repetitive maintenance work.

Dreame’s expansion has a wider radius. Robot vacuums, wet-dry cleaners, robotic mowers and pool cleaners share an obvious cleaning or robotic connection. Hair dryers, kitchen appliances, air treatment, wearables and smart vehicles make the portfolio harder to describe as a single category system. Dreame is asking the market to accept a technology-company identity broad enough to connect them.

That produces two different tests.

Roborock has to prove that adjacency creates a real second growth curve without eroding the economics of its core. Dreame has to prove that technological reuse can overcome the commercial differences between categories.

A robotic lawn mower is not distributed or serviced like a robot vacuum. A pool cleaner has different seasonality, waterproofing and repair requirements. Major kitchen appliances create installation and after-sales obligations. Smart vehicles operate on an entirely different regulatory, capital and safety scale.

The further a company moves from its core, the less useful a shared motor, algorithm or brand story becomes on its own.

Product Innovation Is Only the Visible Layer

The two companies are often compared through visible product launches because those are easy to photograph and measure.

Roborock built much of its reputation on navigation, mapping, software integration and a progression from standalone robot vacuums to increasingly automated docks. More recent products have emphasized lower bodies, obstacle handling, anti-tangle systems and mechanical structures. Its Qrevo family also expanded price coverage, allowing Roborock to compete across more of the market rather than reserve the brand for a narrow flagship tier.

Dreame’s product language is more aggressive. It highlights high suction numbers, robotic legs, extendable cleaning structures, hot-water or steam systems and rapid launches across multiple price bands. Its 2026 communications explicitly describe bionic robotic arms and other technologies as platforms that can migrate into different appliances.

For industry partners, however, the important question is not who announces the more dramatic feature. It is whether that feature can be industrialized with stable quality, controlled cost and acceptable service exposure.

High product velocity can improve shelf visibility and allow a brand to enter new price bands quickly. It can also shorten product life cycles, complicate spare-parts planning and leave distributors holding older inventory. A more concentrated portfolio may be easier to forecast and support, but it can lose attention when competitors reset specifications faster.

Innovation speed and operating quality are not opposites. The difficult task is maintaining both as the portfolio grows.

Globalization: Coverage Is Not the Same as Operating Quality

Roborock and Dreame are both global brands, but the available evidence describes their globalization differently.

Roborock’s annual report provides a financial view. Overseas main-business revenue exceeded RMB10 billion in 2025 and grew faster than domestic revenue. Direct sales and distribution were both material, showing that Roborock is not relying on a single route to market. The company also disclosed rising spending on brand promotion and self-operated global channels.

Dreame’s announcements provide a footprint view: countries entered, stores opened, units shipped and markets in which it says the brand holds leading positions. This communicates speed and presence, but it does not show the profitability, inventory position or service cost behind that footprint.

For a distributor, supplier or retail partner, these measures answer different questions.

Country coverage shows ambition. Revenue shows scale. Margin shows economic quality. Inventory shows whether the channel is absorbing products. Service capacity shows whether a brand can protect its reputation after the sale.

The next stage of Chinese cleaning-brand globalization will be decided less by how many markets appear on a map and more by whether the operating system behind those markets remains healthy.

The Transparency Gap Is Part of the Comparison

It is tempting to ask which company is larger. There is no clean public answer.

Roborock publishes audited revenue, product mix, regional revenue, channel structure, margins, expenses, inventory and cash flow. Dreame is private and releases a different kind of information: shipment milestones, retail rankings, store counts, technology claims and product-launch plans.

The estimate of approximately RMB30 billion in 2025 group sales suggests that Dreame has reached substantial scale. It still cannot be treated as a like-for-like comparison with Roborock’s RMB18.695 billion in audited revenue: the Dreame number is an external estimate, its accounting perimeter is not publicly defined and no accompanying audited profit, inventory or cash-flow statement is available.

Putting those figures into a single ranking would create false precision. Revenue is not GMV. Shipment is not retail sale. A global ranking for one quarter is not the same as full-year market share. A premium-segment ranking is not the same as the whole market.

The transparency gap does not prove that one company is stronger. It changes the questions that partners should ask.

Roborock’s weakness is visible: lower margins, higher selling costs, inventory and cash-flow pressure can be tracked. Dreame’s weaknesses are harder to quantify publicly, so partners must rely more heavily on regional sell-through, return rates, payment terms, spare-parts availability and local service performance.

What Suppliers, Retailers and Distributors Should Watch

For industry partners, the Roborock vs Dreame decision should not be reduced to brand popularity.

1. Portfolio discipline

How many SKUs will enter the market, how long will each remain active, and how will old inventory be protected when the next generation arrives?

2. Channel economics

Does the brand maintain consistent pricing across its direct store, Amazon, national retailers and distributors? Rapid global expansion becomes destructive if channel conflict absorbs the available margin.

3. Service infrastructure

Robot vacuums already require batteries, docks, pumps, sensors, brushes and software support. Lawn mowers, pool cleaners and major appliances make service more local and more complex. Spare parts and repair turnaround can matter more than another launch event.

4. Category commitment

Is a new category a long-term business with product road maps and service investment, or a short-term attempt to capture attention? Suppliers and distributors carry the cost when experiments are abandoned.

5. Data quality

Partners should separate audited disclosure, third-party market research, company-reported milestones and strategic forecasts. All four are useful, but they should not be treated as the same kind of evidence.

Which Strategy Is More Defensible?

Roborock’s model is more legible. Robot vacuums remain the core, overseas revenue is substantial, and the financial effects of diversification can be measured. Its challenge is that a visible operating model is not automatically a comfortable one. The company’s 2025 growth came with falling profit and margin pressure, showing that global scale and category expansion can weaken the economics that made the core attractive.

Dreame’s model has a larger theoretical ceiling. If the company can repeatedly transfer engineering, supply-chain and brand capabilities into new categories, it could become far more than a cleaning-appliance company. But every additional category increases the number of commercial systems Dreame must master. Product engineering is only one of them.

The answer therefore depends on the industry environment.

When new categories are forming and technology resets are frequent, Dreame’s speed and breadth can create more opportunities. When markets mature and competition shifts toward margin, inventory, service and channel stability, Roborock’s more measurable operating discipline becomes more valuable.

Neither route is inherently safer. Focus can become dependence. Expansion can become complexity.

Final View

Roborock and Dreame represent two versions of the next Chinese global technology company.

Roborock is testing whether a company can turn leadership in a mature robot-vacuum category into a broader home-maintenance business without losing financial quality. Dreame is testing whether the engineering system built around cleaning can support a much larger intelligent-living platform.

The winner will not be determined by a single flagship, suction number or exhibition launch. It will be determined by whether expansion produces durable revenue, healthy channels, manageable inventories, reliable service and a brand that customers and partners can still understand.

That is why the most important Roborock vs Dreame comparison is not about which robot cleans a floor better. It is about which company can keep its operating system coherent while its ambitions grow.

Frequently Asked Questions

Are Roborock and Dreame owned by Xiaomi?

No. Both companies have historical links to the Xiaomi ecosystem, but they operate as independent businesses and brands. Roborock is a publicly listed company. Dreame is privately held.

Which company is bigger, Roborock or Dreame?

There is no reliable like-for-like public comparison. Roborock reported audited 2025 revenue of RMB18.695 billion. Public estimates place Dreame’s 2025 group sales at approximately RMB30 billion, but Dreame does not publish an equivalent audited annual report. The estimate indicates scale; it does not support a precise financial ranking.

Which company is more diversified?

Dreame currently presents the broader portfolio and strategic vision, extending from cleaning into major appliances, personal care, outdoor robotics and smart mobility. Roborock is also diversifying, but its expansion remains more closely connected to home cleaning, laundry and autonomous maintenance.

Which brand leads the global robot-vacuum market?

The answer depends on the period and measurement. A Roborock listing document citing Frost & Sullivan ranked Roborock first globally by robot-vacuum GMV and sales volume in 2024. Dreame said, citing IDC, that it ranked first by global robot-vacuum unit sales and revenue in the first quarter of 2026. These are different periods and research methodologies, so they should not be presented as a direct contradiction.