- Roborock’s early success came from timing, technology, Xiaomi, and product quality.

- After 2020, those advantages weakened as Ecovacs, Tineco, Narwal and others accelerated.

- The author argues Roborock entered 2022 at a historical crossroads.

In May 2021, stock investors suddenly discovered that a company on the ChiNext board had a share price above RMB 1,000. At its peak it once approached RMB 1,500, close to the share price of Kweichow Moutai, China's leading baijiu company. For a while, Roborock became an object of public curiosity. As people learned more about Roborock, titles such as the “Moutai of robot vacuums” and the “Moutai of machines” were attached to it.

By 2022, Roborock's share price had fallen to more than RMB 800, with a market value of more than RMB 50 billion, behind old rival Ecovacs at more than RMB 70 billion. If one looks only at market value, the gap does not seem large. But with deeper analysis, one may find that the gap between the two has already widened significantly, and judging from subsequent development, it may widen further.

Let us look at the sales changes of the two companies in recent years:

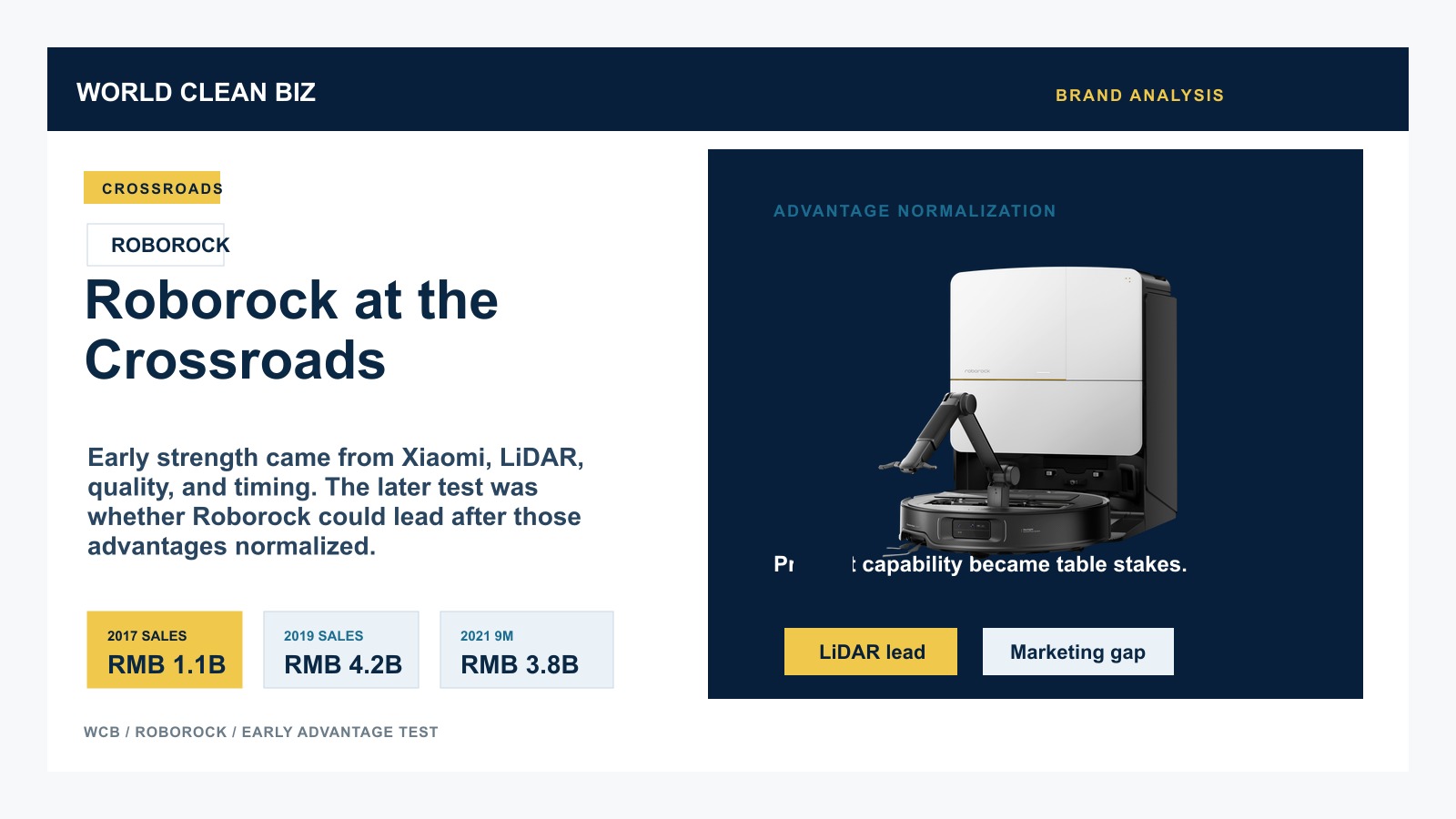

In 2017, Roborock's sales were RMB 1.119 billion, while Ecovacs' sales were RMB 4.55 billion.

In 2018, Roborock's sales were RMB 3.051 billion, while Ecovacs' sales were RMB 5.694 billion.

In 2019, Roborock's sales were RMB 4.205 billion, while Ecovacs' sales were RMB 5.312 billion.

In 2020, Roborock's sales were RMB 4.530 billion, while Ecovacs' sales were RMB 7.234 billion.

In the first three quarters of 2021, Roborock's sales were RMB 3.827 billion, while Ecovacs' sales were RMB 8.244 billion.

One can see that Roborock grew very rapidly in its early years. But in 2020, Ecovacs' sales suddenly surged and pulled far ahead of Roborock. What happened here?

Roborock was founded by Chang Jing, a former Baidu product manager, and received investment from Xiaomi. At the beginning of the company, it relied on strength that crushed the industry and solid product quality, and soon after launch became an industry leader. Roborock's early development was phenomenal mainly for the following reasons.

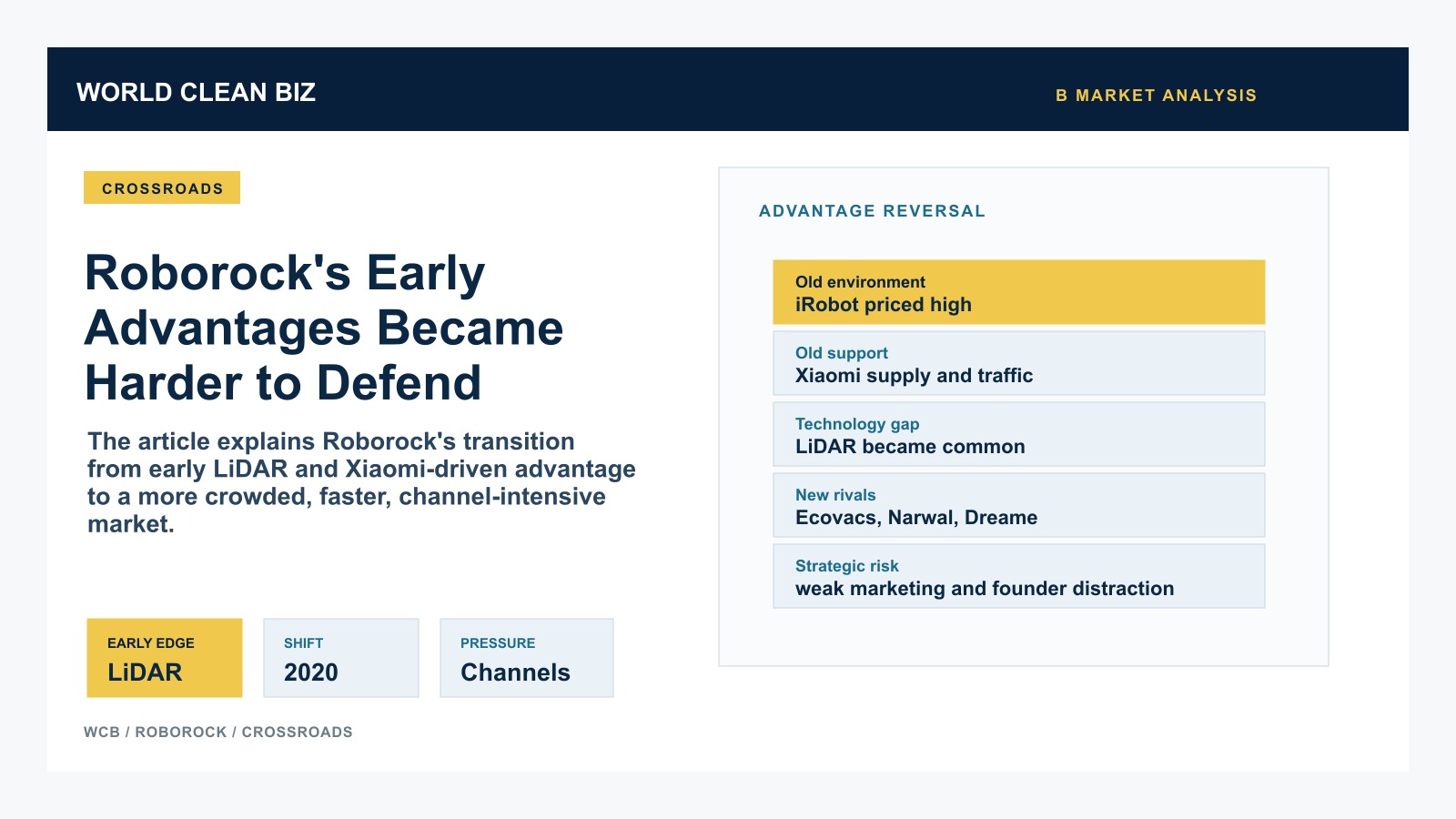

- External environment. At that time, iRobot's products in the market were very expensive. Even ordinary random-navigation machines cost RMB 2,000 to 3,000. Domestic companies were still struggling, and their main shipments were still random-navigation and gyroscope-navigation products that were not very smart. Laser modules were very expensive, and LiDAR navigation products were nearly RMB 4,000. Relying directly on Xiaomi's powerful supply chain, Roborock obtained laser modules at very good prices. Its first LiDAR navigation product was priced at RMB 1,500. With Xiaomi's powerful sales channel, Roborock achieved huge success in its first year.

- Technical strength. In people's impression, Roborock is a technology-focused company with ordinary marketing. In the company's early stage, Roborock had few marketing and sales people; many team members were R&D staff and engineers. In navigation algorithms, Roborock could be said to comprehensively crush the entire industry in its early days.

- Xiaomi's support. Without Xiaomi's support, Roborock could not have obtained such cheap LiDAR navigation modules. In addition, without Xiaomi's strong early sales capability, a company like Roborock, whose marketing was relatively weak, probably could not have sold such large volumes early on.

- Craftsmanship. Before Roborock and Xiaomi launched the robot vacuum, robot vacuums had a reputation among consumers as toys and as impractical products. Quality was also poor. Roborock and Xiaomi jointly raised industry quality by several levels.

These were the reasons for Roborock's success. But the source of profit and loss is often the same: where one succeeds is also where one later suffers setbacks.

After Roborock became one of the industry leaders, the external environment, competitors, and market structure all changed substantially. The turning point occurred in 2020.

If we now review Roborock's early advantages, many of them have disappeared.

- External environment. The market leader is no longer iRobot, but Ecovacs, Xiaomi, Roborock, and Narwal. These companies' R&D innovation capability and product-iteration execution are not comparable to iRobot in its early years. Product prices in the market entered the red-ocean stage long ago.

- Technical strength. By 2020, and even in the years before that, the industry had already completed adoption of LiDAR navigation technology, and LiDAR module prices had fallen sharply. Third-party suppliers in the industry, such as EAI and LD Robot, already had mature LiDAR navigation technologies, with little difference from Roborock and others. Ecovacs had also completed its own self-developed LiDAR navigation algorithm layout early. Roborock no longer has much lead over other competitors.

- Xiaomi's support. For its own development, Roborock no longer manufactures Mijia-brand vacuum cleaners for Xiaomi and focuses mainly on development of the Roborock brand. This has both advantages and disadvantages.

- Craftsmanship. Obsessing over details is good for products. But sometimes, if one becomes too entangled in unnecessary details, one may miss major industry opportunities. Narwal's self-cleaning robot vacuum and Tineco's hard floor washer both had major quality issues from a product perspective, but consumers in the market accepted them. What mattered more was getting the product out first.

The core reason Ecovacs began to lead Roborock by a large margin from 2020 was the explosion of Tineco hard floor washers, a sub-brand of Ecovacs. Riding the tailwinds of the pandemic, livestreaming, and short video, Tineco hard floor washers swept all channels and became synonymous with the hard floor washer category.

For Ecovacs and Tineco, one can refer to my article “Ecovacs at the Crossroads.”

If we analyze Roborock's product line in depth, we can see that the competitive pressure it faces will not be small.

Robot vacuums:

- Home robot vacuums. Roborock-brand robot vacuums count as high-end products in the category. But high-end status cannot rely only on price. Product innovation and functionality are also very important. In 2020, Narwal suddenly emerged and surpassed Roborock in high-end robot vacuums. Its single product approached RMB 2 billion in sales and led the robot vacuum industry toward self-cleaning.

In September 2021, Ecovacs released the full-function robot vacuum X1, once again pushing the industry into an arms race.

Although Roborock released similar products after Narwal J1 and Ecovacs X1, its role had shifted from industry leader to one of the followers.

Although Roborock is still a leader in robot vacuums, from a product perspective, no current innovation seems to be led by Roborock.

At the same time, robot vacuum competitors continue to increase. Narwal, valued at RMB 30 billion; Dreame, valued at RMB 17 billion; the new Beetl and increasingly capable robot vacuum players are all challenging Roborock's leading position.

- Commercial robot vacuums. This market is too small. Whether Ecovacs or Roborock, this area can temporarily be ignored.

- Hard floor washers. Tineco is currently synonymous with the hard floor washer category and holds 60% of the China market. Roborock also has a hard floor washer, the U10, but to be honest, its sales volume is on a completely different order of magnitude. Although the U10 has some innovation, the industry is iterating continuously, and Tineco's iteration speed has far exceeded that of the rest of the industry. It is foreseeable that Roborock will not be able to squeeze into the top ranks of the hard floor washer industry for now.

- Handheld vacuum cleaners. These can basically be ignored.

From a product perspective, Roborock's innovation capability has already declined substantially.

In addition, in marketing and channel layout, Roborock remains as weak as before.

From any perspective, Roborock now faces a more difficult situation than in previous years. If Roborock previously used product quality and technology to offset its marketing weakness, it no longer has that advantage on the product side.

In 2021, Shanghai Rox Intelligent Technology Co., Ltd. was established. At the end of the year, Tencent and Sequoia Capital led a USD 100 million investment. Rumors that Roborock would participate in carmaking finally settled. But the protagonist of the carmaking story changed from Roborock to Chang Jing personally. It is said that Rox Intelligent's car direction is mainly an off-road vehicle similar to the Mercedes-Benz G-Class, using a range-extender route similar to Li Auto. Most of Chang Jing's energy will also be pulled away from Roborock and placed mainly on carmaking.

For Roborock, however, at a time when the robot vacuum industry is facing attacks from many powerful competitors, is it a good thing that the founder leaves the company and turns to another industry? Many years later, after the industry competition structure is settled, people looking back may find that this year was a crossroads for the robot vacuum industry. Who will be the winner reviewing the story then?

In 2022, Roborock stands at a historical crossroads.

For buyers deciding where to compete next, the six robot vacuum product opportunities connect platform choices with households, channels, and verification conditions.