- Narwal’s valuation depends on whether its product differentiation can support long-term scale.

- The company’s strength is tied to self-cleaning and user-maintenance innovation.

- Revival in robot vacuums requires both product credibility and stronger commercial execution.

Denny, Narwal is now valued at 30 billion yuan. Do you think it's worth it?

Do you have any connections with Narwal? Could you help us make a connection to consider co-investing? This was in the peak year of investment in 2021.

From that time frame, Narwal seemed like the most favored company by investors:

- First, founder Zhang Junbin has an academic background, having been admitted directly from primary school through graduate school. The subsequent team members also came from high-tech companies such as Huawei and DJI. Compared to competitors, the talent density is much higher.

- Narwal pioneered self-cleaning floor washers with water tanks, creating a new product category. They made significant innovations in their products, which appeared in a completely new form. Such products require substantial investment and have strong barriers to entry. At that time, there were no competitors in the market. I reported on this product when they launched it through crowdfunding in 2019.

- In terms of marketing and sales for startups, Narwal did exceptionally well. When influencer marketing was still unfamiliar, Narwal extensively promoted their products on platforms like Xiaohongshu and Douyin, capitalizing on the significant benefits these platforms offered. ByteDance also strategically invested in Narwal, providing additional resources. In 2019, they received millions of orders just after launching during the Double Eleven event. By 2020, as Xiaohongshu and Douyin grew, their annual sales reached over one billion yuan.

- Regarding financing, Narwal secured investments from DJI's shareholder Professor Li Zexiang early on and later from ByteDance’s strategic investment. Subsequent rounds of funding saw investors lining up to offer money, indicating that the company was not in need of funds.

- The external environment for cleaning appliances was very favorable. Roborock reached a market value of 100 billion yuan in 2021, while Ecovacs also saw its stock price increase by 27 times due to Tineco's growth. All consumer-focused investors were searching for the next target. With Narwal’s sales approaching half of Roborock’s original industry giants’ sales and Roborock’s peak market value reaching nearly 100 billion yuan in 2021, a valuation of 30 billion yuan was quite reasonable.

All these advantages made it hard not to be excited about Narwal becoming the next Roborock, potentially going public and achieving career success.

However, all gifts from fate come with a price tag.

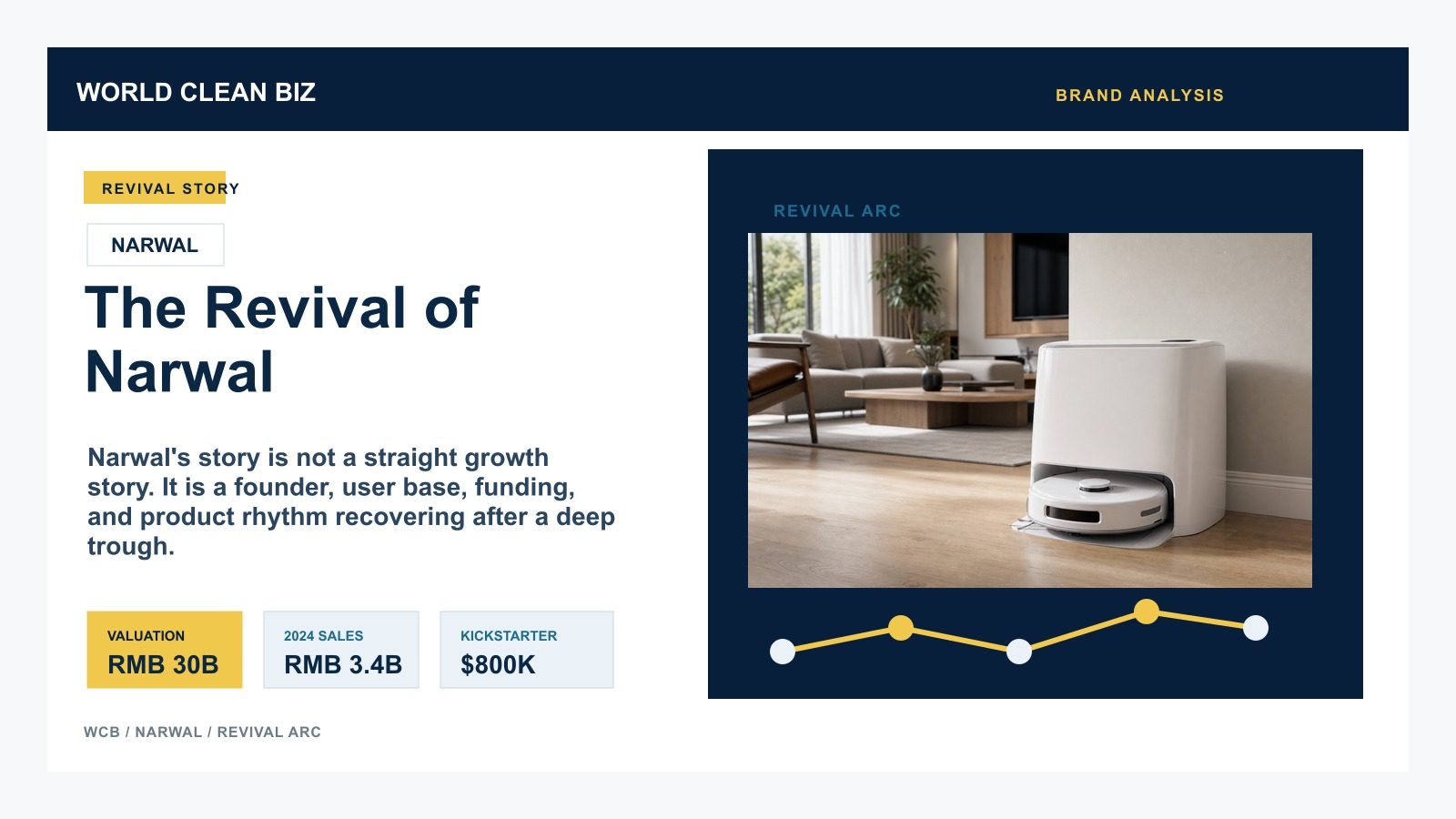

After reaching its peak in 2021, Narwal experienced a sharp decline in sales, product obsolescence, key team members leaving, and entered a dark period lasting nearly three years.

These issues had early signs but were overshadowed by the impressive sales figures of 2020-2021.

Several critical issues:

- Narwal built factories from the outset when its brand products were still not fully established. Building factories before the product line was smooth for a startup is not an ideal decision. Factories require significant physical and detailed work, which was not the strength of the initial Narwal team, diverting much of their founders' energy.

- The team was too young with little industry experience. Their first product's huge success led to a sense of invincibility among the team, causing them to undervalue competitors in the industry. Consequently, they launched many projects like cat litter boxes and floor washers. Many people from Huawei and DJI joined the team. At that time, Narwal’s only competitor might have been DJI.

- Product-wise, their first product was innovative but not well-received by the market. Many suppliers were uncooperative. A senior executive at Xiaomi told me that they rejected Narwal's request due to perceived flaws in the product and expected high return rates. I remember many complaints about poor navigation algorithms causing the device to get stuck.

Narwal’s CEO also mentioned that in 2021, their products had tens of thousands of issues where they couldn’t move at all. After spending half a month fixing them, they sent the devices back to customers, which was a crisis for the company. He thought the company might have to shut down.

Additionally, J1 could not perform both vacuuming and mopping simultaneously; one needed to manually switch the mop head on.

Moreover, there were significant misalignments in product development with market trends. After Ecovacs’ X1 launched in 2021, the industry shifted towards all-in-one docks. However, Narwal did not release its all-in-one dock J4 until 2023.

- Competitors. When Narwal first released J1, no one was optimistic about this product. But once sales figures came out, they never missed a beat. Roborock and Ecovacs quickly launched similar products that were even better. Ecovacs also launched the X1 with vacuuming, mopping, and other all-in-one docks in late 2021, followed by Roborock’s similar product launch half a year later, which ignited the robot vacuum market. The industry entered an era of all-in-one docks, with everyone entering this space. Narwal went from having no competitors to being crowded out.

- Financing. Narwal rejected several funding opportunities that gave Dreame a chance. Yu Hao of Dreame seized this window period and raised 3.6 billion yuan in financing, setting a record for the industry. With this money, Dreame initiated a price war in the cleaning appliance market. Without Dreame, the current competitive landscape of cleaning appliances would be very different.

- Patents. Narwal's products are highly innovative, but they lack adequate patent protection. This has allowed competitors to quickly follow and surpass them. A friend once told me that the value of Narwal’s patents is at least 1 billion yuan.

- Going Global. Narwal initiated a Kickstarter campaign in 2019, raising nearly $800,000. One would expect this to provide some experience for the overseas market. However, they did not launch their products internationally until 2023, missing out on significant changes in the global market that year. In contrast, Dreame and Roborock also began their international expansion around 2019, with overseas markets becoming a key growth and profit driver for these companies.

- Marketing Channels. From 2019 to 2020, platforms like Xiaohongshu and Douyin were a significant source of growth dividends. Narwal's success was closely tied to this period. However, once competitors entered the market, these channels became purely about spending money to achieve return on investment.

Thus, during 2022-2023, as all these issues came to a head, Narwal experienced a significant decline in sales, with many team members leaving. What was once an unattainable company now seemed within reach for anyone. It's easy to imagine the immense pressure faced by the founder.

It wasn't until 2023 when Narwal launched its all-in-one dock J4 and Freo 001 that they began to regain their footing. With product capabilities catching up with industry standards, Narwal benefited from government subsidies in 2024, leading to a new surge in growth. It is rumored that Narwal's sales reached 3.4 billion yuan in 2024, indicating a revival and the ability to compete head-to-head with any competitor.

Most companies facing such challenges struggle to recover, but Narwal managed to overcome its difficulties for three main reasons:

Firstly, the founder. As Roger Ye once said, as long as a company's founder doesn't want it to end, the company is hard to shut down. Investors will find various resources to keep the company alive unless the founder loses their drive. After reviewing some of Narwal’s CEO's interviews, I noticed that his demeanor had become more gentle, but his inner strength and grounded perspective on the industry had grown. The product development process also became more rhythmic. A founder is a company's greatest moat; one who hasn't experienced life-and-death struggles cannot truly grow. From this perspective, I am optimistic about Narwal’s future.

Secondly, users. Although Narwal's early products had many issues, they also gained a loyal user base. These users continued to prioritize Narwal during product updates and upgrades. In 2022, it was somewhat surprising that even with the all-in-one dock already in place, many users still chose Narwal’s models without dust collection functions. These users have become valuable assets for Narwal's comeback.

Lastly, funding. Regardless of any other considerations, if sales were declining and there wasn't sufficient capital, Narwal likely wouldn’t have survived the intense competition from major players. Narwal secured additional rounds of funding to ensure adequate resources.

The cleaning appliance industry has experienced a tumultuous development over recent years. Narwal's growth trajectory is particularly emblematic—from an initial rapid rise, through a trough, and back to a challenge against industry giants, demonstrating remarkable resilience throughout.