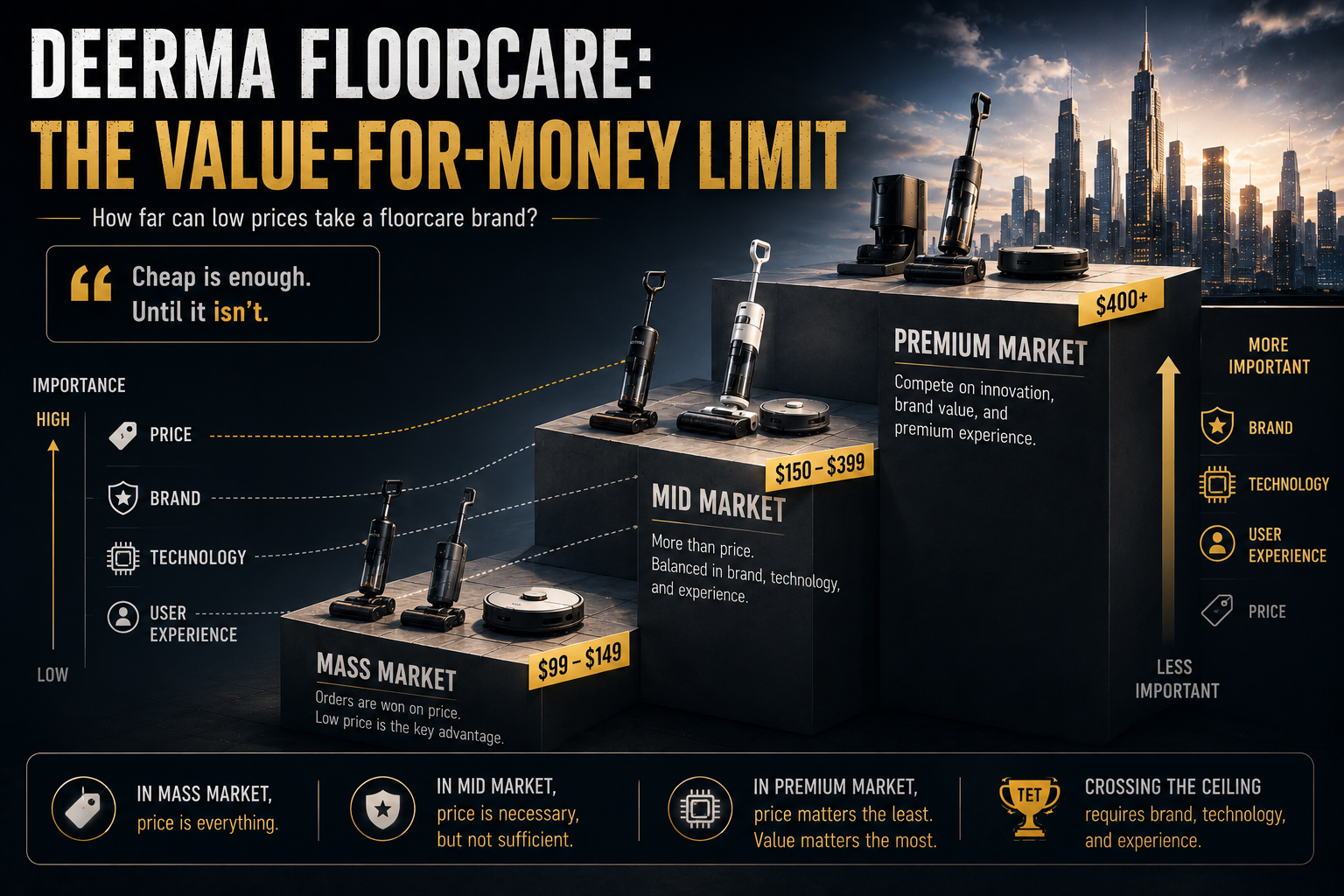

- Deerma’s challenge reflects a broader limit of the value-for-money model in complex floorcare categories.

- Robot vacuums and hard floor washers require R&D, after-sales control and channel profit, not only low prices.

- Deerma’s remaining opportunity may be in overseas mass-market channels and clearer subcategories.

Preserving the paragraph meaning and standard names as requested, but no numbers, URLs, or data were present in the original text to maintain.

Over the past decade, high cost-effectiveness has been one of the most effective strategies in Chinese consumer hardware.

Xiaomireshapeded many categories with "high configuration, low price, and strong traffic," benefiting a batch of ecosystem and small appliance companies.Deerma was among them. Before entering Xiaomi's ecosystem, it already excelled in design, low pricing, and e-commerce operations; later, working for Xiaomi strengthened its supply chain, product selection, and online channel capabilities.

This set of abilities was very effective during the era of ordinary small appliances. Deerma’s forte was not creating products with high technical barriers but finding mass-market needs, making products look good, cheap, and sufficient, and quickly selling them through online channels.

But cleaning appliances did not follow this logic. Especially for core categories like robotic vacuums and floor cleaners, the competition was no longer about who could make a product cheaper, but who could continuously invest in R&D, control after-sales service, ensure channel profitability, and establish clear category mindsets.

The most misleading aspect of cleaning appliances to outsiders is that they appear similar to small appliances but are actually complex hardware businesses requiring significant R&D investment, strong channels, robust after-sales support, and long-term iterative improvements. Deerma's predicament was a typical example of this change.

In 2020, Tineco's floor cleaner became an industry phenomenon, one of the few breakout products in cleaning appliances.

For several years, there was a clear sentiment in the industry. Many friends from large companies told me something similar: "Denny, our company has made washing machines a strategic priority; we must seize this opportunity."

This excitement wasn't just about individual companies but an industry-wide reaction. Many small appliance makers, vacuum cleaner manufacturers, motor producers, contract manufacturers, and e-commerce channel players were all looking at floor cleaners. When these companies internally initiated projects, they didn’t first ask if they had the capability; instead, they asked if not doing so would mean missing out on the next Tineco.

In recent years, hundreds of billions of dollars have flooded into the cleaning industry. This wave of investment reached its peak when Dreame raised RMB 3.6 billion in funding. Deerma was a significant participant in that wave.

It wasn't just a simple test but a serious commitment. Deerma established a team of several dozen researchers in Suzhou, with competitive salaries. Suzhou is one of the regions most concentrated with cleaning appliance supply chains and R&D talent. Deerma's headquarters are in Guangdong, where small appliance supply chains are well-developed, but the density of robotic vacuum and floor cleaner talent is much lower than in Suzhou.

Deerma’s move to establish a team in Suzhou was essentially about getting closer to the cleaning appliance supply chain and filling its past gaps in R&D and industrial resources within the small appliance model.

At that time, Deerma's strategy was clear: using its familiar cost-effectiveness approach to capture the low-price floor cleaner market.

Tineco’s and Dreame’s hard floor washers mainly competed above the 2000 yuan price point. Deerma launched several models, including a wired version for around 800 yuan and an untethered model priced just over 1000 yuan. This strategy was not out of line at the time. From 2020 to 2021, Tineco's brand sales grew from zero to nearly ten billion yuan, a significant opportunity for all small appliance companies.

At that time, there was a consensus in the industry: if floor cleaners were to rapidly penetrate the market like robotic vacuums, low-price segments would eventually open up. Deerma aimed not just at selling several products but establishing user mindshare for low-price floor cleaners.

Floor cleaners also created an illusion for many companies: this was a high-margin, high-growth new category.

Previously, a businessman from a company with over 1 billion yuan in scale came to me seeking entry into the hard floor washer market. He calculated that MOVA's hard floor washers sell for more than 3,000 yuan, with costs under 1,000 yuan. If he sold them for 2,000 yuan each, making a profit of 1,000 yuan per unit, selling 200,000 units in a year would yield a profit of 200 million yuan.

This calculation sounds enticing, but it overlooks the critical operating costs associated with hard floor washers. At that time, I detailed for him the platform fees, promotional expenses, after-sales service, and potential return rates as high as over 30%. In the end, I told him that if he truly wanted to enter the hard floor washer market, the starting threshold would be at least one billion yuan.

The most misunderstood aspect of hard floor washers is seeing only sales figures without considering operating costs. Once this category enters a price war, margins are already thin, and adding returns, repairs, advertising, and after-sales service makes it even harder to calculate profits as more products are sold.

Deerma's issue lies here as well. It excels in e-commerce operations, product selection, supply chain integration, and defining cost-effective products. However, robot vacuum and hard floor washer are not merely about simple product selection; they require significant R&D investment, deep supply chain integration, and robust after-sales service. Especially for the hard floor washer, entering the price-sensitive segment limits gross margin potential. If return rates and after-sales pressures increase, the financials become even more challenging to manage.

By 2026, the industry gap has become evident.

Dreame's sales have reached over 30 billion yuan, while Roborock is close to 20 billion yuan, and Ecovacs is also close to RMB 20 billion yuan. According to the reporting scope for 2025, Deerma's total revenue is 3.432 billion yuan, with home environment-related income from cleaning appliances amounting to approximately 1.234 billion yuan, a decrease of 10.78% year-over-year, and a gross margin of 20.70%.

Clean-related revenues exceeding 1.2 billion yuan indicate that Deerma does have a cleaning business. However, compared to leading companies, it more resembles a small appliance company with a cleaning segment rather than a platform-focused cleaning appliance company.

Robot vacuums and hard floor washers subsequently formed very narrow brand-dominated markets. Robot vacuums are primarily dominated by Ecovacs, Roborock, and DREAME; hard floor washers are mainly represented by TINECO, DREAME, and Roborock. Deerma failed to establish itself as a leading brand in either category—neither did it define the robot vacuum market nor become a representative brand in the hard floor washer segment. It is not that Deerma lacked products but rather that it failed to capture the category definition.

This indicates that the cost-effective approach did not enable Deerma to enter the main brand market for cleaning appliances. While low prices can provide entry opportunities, they do not automatically establish category awareness and cannot replace R&D, after-sales service, and long-term investments.

This change is not limited to Deerma; Xiaomi's transformation better illustrates the point.

Xiaomi pioneered the high-performance-to-price ratio approach. When its robot vacuum was introduced at 1,499 yuan, it rewrote the industry's pricing framework and brought Roborock to prominence. However, as cleaning appliances have evolved to include all-in-one bases, hard floor washers, AI obstacle avoidance, roller mops, robotic arms, high-end flagship models, and overseas market channel competition, Xiaomi's presence has noticeably diminished.

The value proposition approach requires that the brand itself generates its own traffic, and channels and partners can still make a profit. Cleaning appliances are high in after-sales, service, and explanation costs. If channels do not have sufficient profit margins, it is difficult to sustain sales. Even Xiaomi struggled to maintain its early dominance, indicating that cleaning appliances have imposed systemic boundaries on the value proposition approach.

Uwant provides another answer: E-commerce companies do not necessarily need to demonstrate themselves in robot vacuums and hard floor washers.

Uwant initially relied on e-commerce operations to get started and later secured investment from Gao Hua Capital, entering the cleaning appliance industry on a large scale. Initially, Uwant invested heavily in robotic mops; however, it was actually its dust mite removers that became successful. Later, Uwant's dust mite remover sales reached several million units annually, making it a representative player in itssub-category.

Uwant's success did not stem from its deeper understanding of robotic mops compared to Deerma but rather from its earlier recognition that it was unsuitable for head-to-head competition with Trifo, Dreame, and Roborock in the main market of robotic mops. Dust mite removers are closer to Uwant’s capability boundaries: demand is direct, demonstration effects are strong, product complexity is low, and after-sales pressure is manageable.

This indicates that while affordability and e-commerce capabilities may not be entirely ineffective, they are unsuitable for forcefully entering the main markets of robot vacuums and robotic mops. They are better suited to categories with lower complexity, more manageable after-sales pressure, and clearer scenarios. Deerma's issue lies in its failure to establish a sufficiently clear tag in similar niche scenarios.

Whether Deerma will have opportunities in cleaning appliances in the future depends on its performance in the overseas market.

The domestic market is highly competitive. The landscape for robot vacuum and hard floor washer has largely taken shape, with intense price wars in the mid-to-low-end price segments. Platform fees are high, and channel profits are thin. If Deerma continues to compete directly with Roborock, Ecovacs, Tineco, Narwal, Dreame, MOVA, Aiper, Beatbot, Maytronics, SharkNinja, iRobot, Dyson, Deerma, Uwant, Anker, Xiaomi, Husqvarna, and Positec in the domestic market, it will face significant challenges.

The overseas market is relatively less competitive. Over the past few years, many cross-border e-commerce brands have avoided the domestic price wars and have thrived on platforms like Amazon, independent websites, regional channels, and local distribution systems abroad. Leading cleaning appliance companies are also doing well in this regard; Roborock, Ecovacs, and Tineco can sustain ongoing price wars and new product iterations largely due to better gross margins and cash flows provided by the overseas market.

Deerma's opportunity does not lie in high-end smart cleaning but rather in the overseas mass-market segment. In regions such as Southeast Asia, Eastern Europe, the Middle East, Latin America, there is still demand for basic vacuum cleaners, entry-level wet vacuums, fabric washing machines, and dust extractors. Deerma’s design capabilities, cost-effectiveness, and supply chain efficiency may be more effective in these markets.

However, exporting domestic low-priced products to overseas markets is not straightforward. It requires local channels, product adaptation, after-sales support, certification systems, and brand building. What Deerma truly needs to validate next is not whether it will continue to produce cleaning appliances but rather whether it can establish a business model that turns cost-effectiveness into a combination of channel profits, after-sales service, and repeat purchases in a specific overseas market, price segment, and product category.