- Robot vacuums are moving from niche smart home devices toward household appliance status.

- Roborock, Ecovacs and Dreame remain central players, but DJI and outdoor robotics companies add new uncertainty.

- The next phase will test global channels, after-sales service and system-level execution, not only product launches.

The robot vacuum market is entering another round of competition. The first stage was about proving demand. The second stage was about navigation, mapping and basic cleaning performance. The third stage was the rise of docking stations. Now the industry is moving toward a more complex phase: higher automation, lower maintenance, global channel competition and the search for a second growth curve.

This is why the market feels calm on the surface but tense underneath. The leading players are stronger than before, but the next battle has not been decided.

The Market Is Still Growing

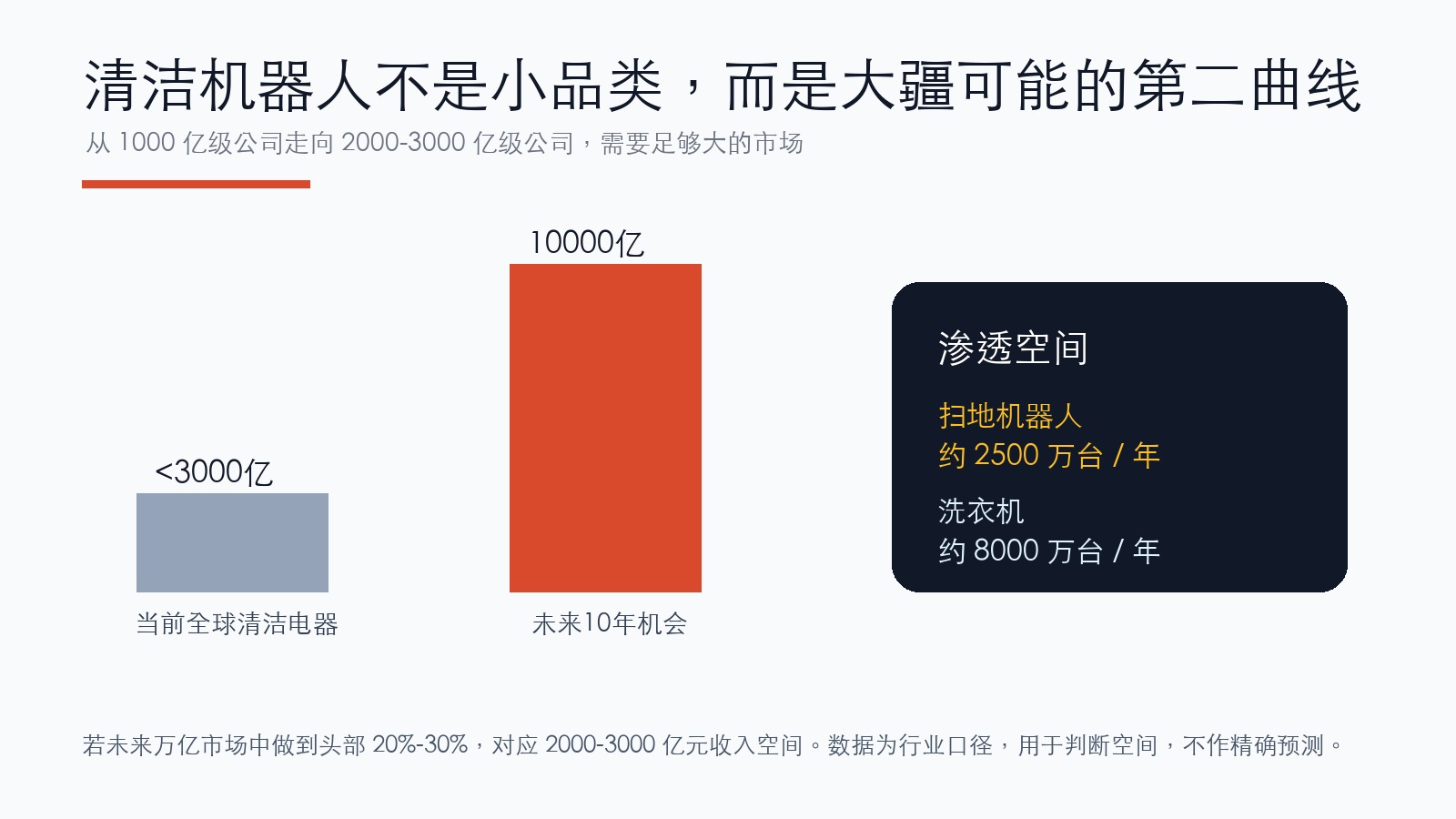

Roborock’s listing materials cited a clear growth outlook: global robot vacuum shipments were about 20.6 million units in 2024, with market value around USD 9.3 billion. By 2029, the market is expected to reach 43.2 million units and USD 25.2 billion.

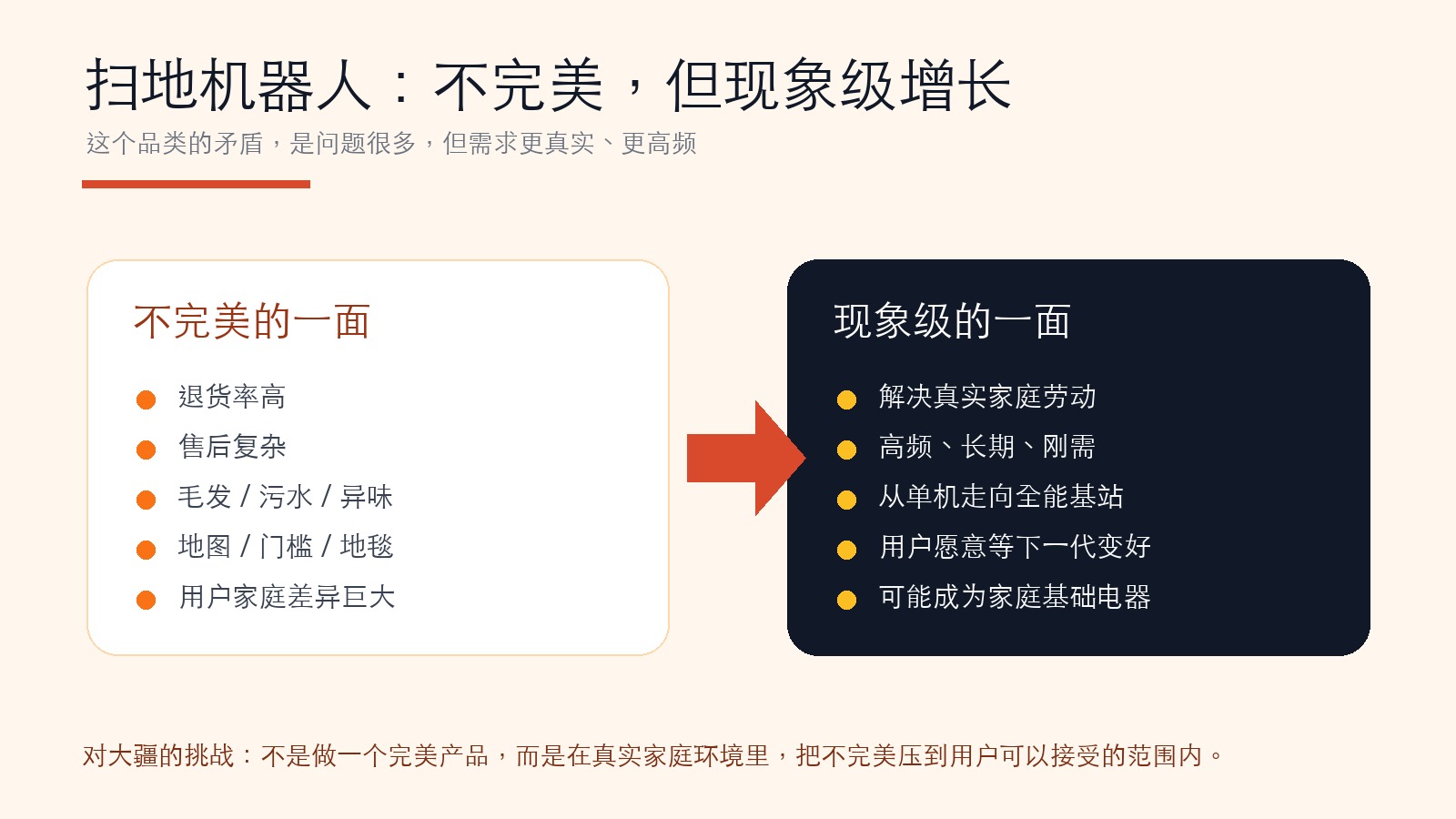

The direction is obvious. Robot vacuums are no longer a niche smart home product. They are moving toward a household appliance category. But the market is not growing evenly. Premium robot vacuums with full-function docking stations are taking value share, while entry-level products face more price pressure.

That creates a difficult balance. Companies need to push higher-end products to protect margins, but they also need volume to support supply chains, app ecosystems, after-sales networks and global expansion.

Roborock Has Become the Benchmark

Roborock is now one of the strongest global robot vacuum brands. It has product depth, a stable team, strong overseas channels and capital market support. In many markets, it has become the reference brand for premium robot vacuums.

Its challenge is not whether it can continue to sell robot vacuums. The bigger question is whether robot vacuums alone can support its next stage of growth. The company needs a second curve. Backyard robotics, including robotic mowers, is one of the more logical directions.

This is why Roborock’s expansion outside indoor cleaning matters. A mature robot vacuum company cannot only defend its current market. It has to use its technology, supply chain and brand assets to enter adjacent robotic categories.

Ecovacs Has Recovered, but the Pressure Remains

Ecovacs has gone through a difficult period, but it remains one of the core players in global floorcare. Its structure is different from Roborock. Ecovacs has both the Ecovacs robot vacuum brand and Tineco, which became one of the most important hard floor washer brands.

This gives Ecovacs a wider cleaning appliance portfolio. It also creates management complexity. Robot vacuums and hard floor washers are different products, with different users, after-sales problems and competitive logic.

Ecovacs’ future depends on whether it can keep both businesses competitive while preventing internal resources from being stretched too thin.

Dreame, Narwal, DJI and Others Change the Table

Dreame has become one of the most aggressive players in cleaning appliances. It competes across robot vacuums, hard floor washers, vacuums and new outdoor categories. Its advantage is speed and willingness to invest heavily in new products.

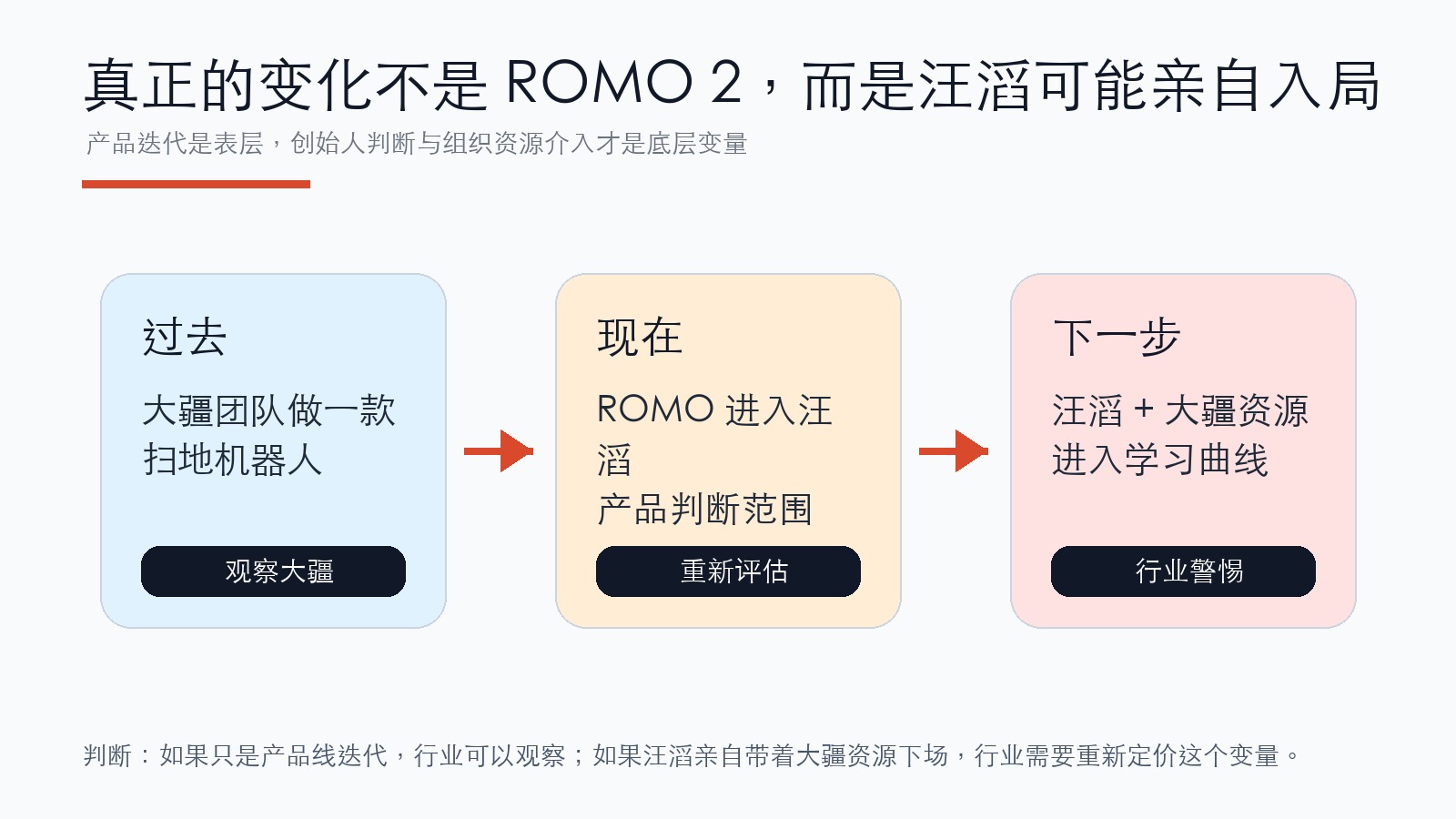

Narwal has built a distinctive position around mopping and docking systems. DJI is a newer but more sensitive variable. If DJI continues to invest in robot vacuums and Wang Tao remains personally involved, the industry will have to face a different kind of competitor: one with strong engineering capability, brand power and a large company resource base.

The next robot vacuum war will not only be between traditional cleaning brands. It may involve outdoor robotics companies, pool robotics companies and strong consumer hardware companies entering indoor cleaning.

The Category Is Becoming a Platform

The robot vacuum is becoming less like a single product and more like a home robotics platform. It combines sensors, motors, pumps, software, mapping, docking stations, consumables and service.

That makes the industry harder for small brands. Product cycles are faster, technology requirements are higher, and after-sales expectations are more demanding. At the same time, the market remains attractive enough to keep drawing new players in.

The next phase will test more than product launches. It will test whether companies can manage global channels, maintain software quality, reduce failure rates, support local service and still keep pricing competitive.

The robot vacuum market before the next war is therefore not an immature market. It is a market that has already created strong leaders, but still has enough growth and uncertainty to change the ranking again.