- Anker's shallow-sea strategy has produced a RMB 30.51 billion global smart-hardware company.

- The company is moving beyond Amazon strength toward a multi-channel global brand system.

- To reach the next stage, Anker must win in heavier categories such as energy storage, smart home and robot vacuums.

Anker Innovations is one of the earliest Chinese consumer-electronics companies to truly break out globally. It started with chargers, power banks, data cables and other 3C accessories, built its brand through overseas e-commerce platforms such as Amazon, and then gradually expanded into earbuds, speakers, projectors, home security, robot vacuums and consumer energy storage.

Anker listed on China’s A-share market in 2020. Now it has submitted an application for an H-share listing in Hong Kong.

The most important thing in this prospectus is not that Anker may have one more listing venue. It is that Yang Meng’s long-discussed “shallow-sea strategy” has, for the first time, become a set of operating numbers that can be tested.

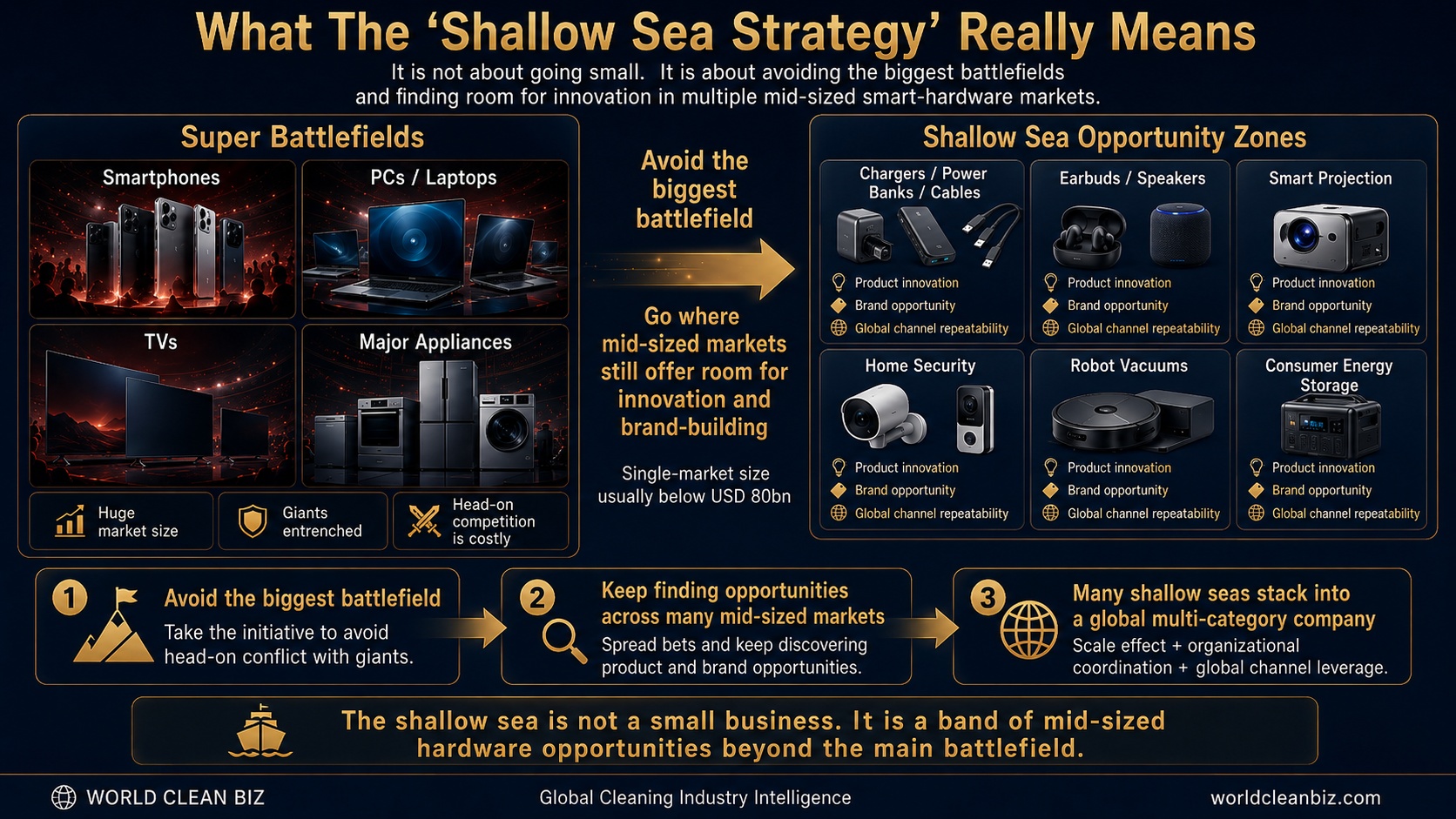

Yang Meng is the founder of Anker Innovations. By “shallow sea,” he does not mean tiny markets. He means mid-sized smart-hardware markets that are smaller than super categories such as smartphones, computers, televisions and major home appliances, but still have room for product innovation and brand-building. In Anker’s prospectus, these markets are defined as markets below RMB 576 billion, or roughly US$80 billion, in size.

This has been Anker’s core operating path over the past decade: avoid the main battlefields where giants deploy their heaviest forces, and keep looking for opportunities in one mid-sized smart-hardware market after another.

Judging from the prospectus, by 2025 at least, this path had already produced results.

Anker is not a small company, nor is it merely a cross-border e-commerce operator that knows how to work platform traffic. In 2025, it reached RMB 30.51 billion in revenue, RMB 2.62 billion in profit, an overall gross margin close to 44%, and nearly RMB 2.9 billion in R&D spending.

For a consumer-hardware company, it is not easy to reach RMB 30 billion in revenue while still maintaining a gross margin above 40%. This suggests that Anker is not relying simply on low prices, broad distribution and platform traffic to exchange for scale. Many cross-border e-commerce companies are shelf businesses, SKU businesses and traffic businesses. What Anker has built is a brand and product portfolio.

This RMB 30 billion revenue base is no longer supported by a single category.

Put simply, Anker is the charging and energy-storage brand; eufy carries home security, cleaning robots and smart home; soundcore is mainly audio; and Nebula is smart projection.

Smart Charging and Energy Storage remains Anker’s largest base. In 2025, it generated RMB 15.40 billion in revenue, accounting for 50.5%. Smart Home generated RMB 8.27 billion, accounting for 27.1%. Smart Audio and Video generated RMB 6.83 billion, accounting for 22.4%. Smart Home and Smart Audio and Video together already contributed nearly half of revenue.

That means Anker is no longer just a charger and power-bank company. It has become a multi-category global smart-hardware company.

This is the real outcome of the shallow-sea strategy.

Shallow seas are not small businesses. In Anker’s prospectus, the upper bound of a single shallow-sea market is about US$80 billion. The point is not to do small markets. The point is not to fight head-on against Apple, Samsung, Haier and Midea in the largest main battlefields.

What Anker has done over the past decade is to keep searching for opportunities in those markets. Chargers, power banks, earbuds, security devices, robot vacuums, smart projectors and consumer energy storage are not the largest categories on their own. But together, they have supported a company with RMB 30 billion in revenue.

What supports this model is Anker’s global channel capability.

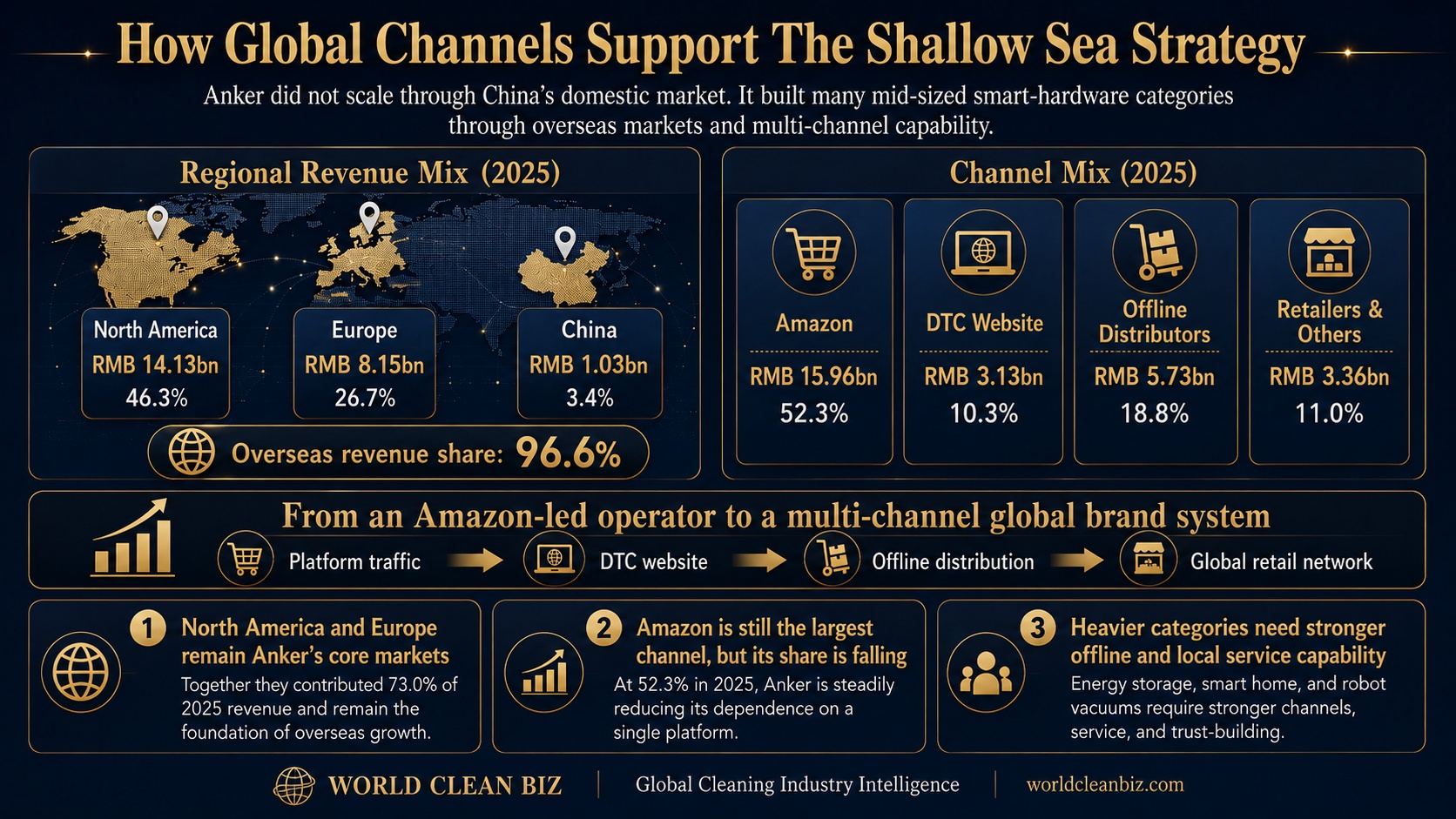

Anker is not a company forged in China’s domestic price war. Its core market has always been overseas, especially North America and Europe. In 2025, overseas markets contributed 96.6% of Anker’s revenue, while China accounted for only 3.4%.

Amazon still contributed more than half of revenue, but its share fell from 57.1% in 2023 to 52.3% in 2025. At the same time, Anker’s own website, offline distributors, retailers and other channels all grew.

This change matters. The more complex the category, the less it can rely on Amazon alone. Energy storage, smart home and robot vacuums all require offline display, local service, regional channels and after-sales systems. Anker is moving from an Amazon-strong operating company toward a multi-channel global brand company.

The business in the prospectus that deserves a separate look is Smart Home.

In 2025, Anker’s Smart Home revenue reached RMB 8.27 billion, with a gross margin of 47.7%, higher than the company’s overall gross margin. eufy Security, eufy Clean and eufyMake correspond to home security, smart cleaning and creative printing. These are typical shallow-sea categories: the markets are not as large as smartphones or televisions, but the demand is real and there is room for product innovation.

The prospectus also says that eufy Robot Vacuum Omni C20 and SoloCam S340 each had gross margins above 50% in 2025. This suggests that eufy’s robot vacuum is not merely a low-margin traffic product. Within Anker’s system, it is part of the Smart Home business, not the entire bet of a cleaning-robot company.

This also helps explain Anker’s repeated trial and adjustment in cleaning appliances over the past few years.

When I previously wrote that “Anker Innovations has no methodology,” I did not mean Anker had no capability. I meant that Amazon, VOC and a boutique-product playbook cannot be copied into every complex category at no cost. Yang Meng’s later emphasis on talent density and the “number one person” in each business was, in essence, a correction to this problem.

The prospectus now proves that Anker has scaled the shallow-sea strategy. But it also shows that the shallow seas are getting heavier.

This is the most realistic side of Anker’s shallow-sea strategy today.

Earlier products such as chargers, power banks, data cables and earbuds were highly competitive, but relatively light. Today’s energy storage, smart home and robot vacuums are heavier in R&D, supply chain, inventory and after-sales service. Anker’s revenue and profit are still growing, but the way it grows has changed.

So the shallow-sea strategy in Anker’s H-share prospectus is both a scorecard and a new exam question.

Before RMB 30 billion, Anker proved that it could keep finding opportunities in shallow seas. After RMB 30 billion, it has to prove that it can fight a hard battle in deeper waters such as energy storage, smart home and robot vacuums.

If it wins, Anker has a chance to move from RMB 30 billion toward RMB 100 billion. If it loses, the shallow-sea strategy will remain a beautiful but limited scorecard.