- The cleaning appliance industry has always been shaped by new product formats, not only stronger brands.

- From Hoover and Electrolux to Dyson, iRobot and Chinese brands, each wave changed the basis of competition.

- The next phase is defined by robotics, wet cleaning, automation and China’s supply chain speed.

The cleaning appliance industry has never moved in a straight line. It has been rebuilt again and again by new product formats, new channels, new manufacturing bases and new definitions of household labor.

The early history of the industry was led by mechanical invention and household adoption. Manual cleaning tools gave way to early vacuum cleaners. Companies such as Bissell, Vorwerk, Nilfisk, Hoover, Electrolux, Miele and later many American and European brands built the first global structure of the category. At that stage, the competition was about mechanical reliability, direct sales, household penetration and the ability to turn cleaning from physical labor into an appliance-driven task.

From Vacuum Cleaner to Consumer Appliance

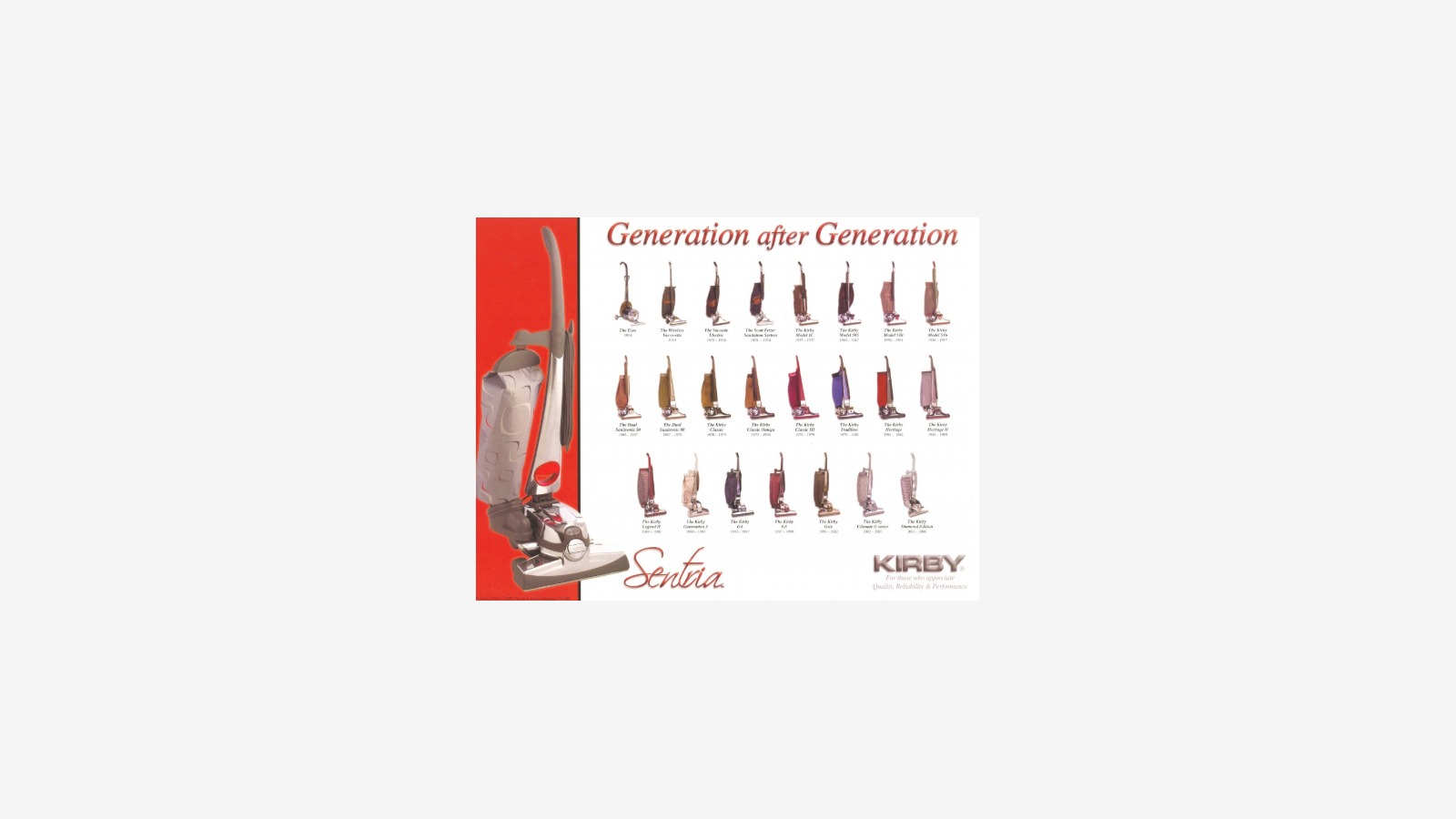

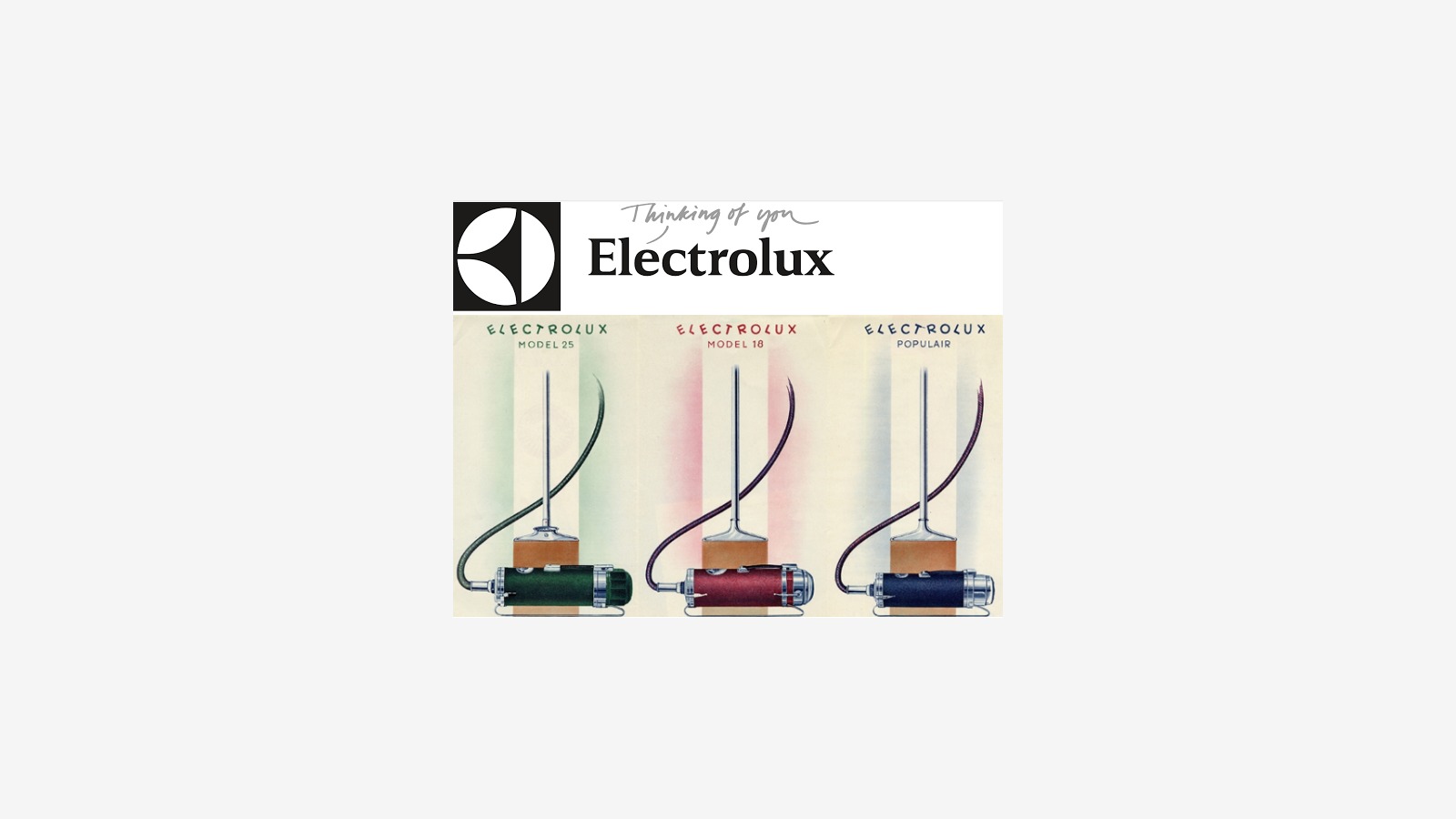

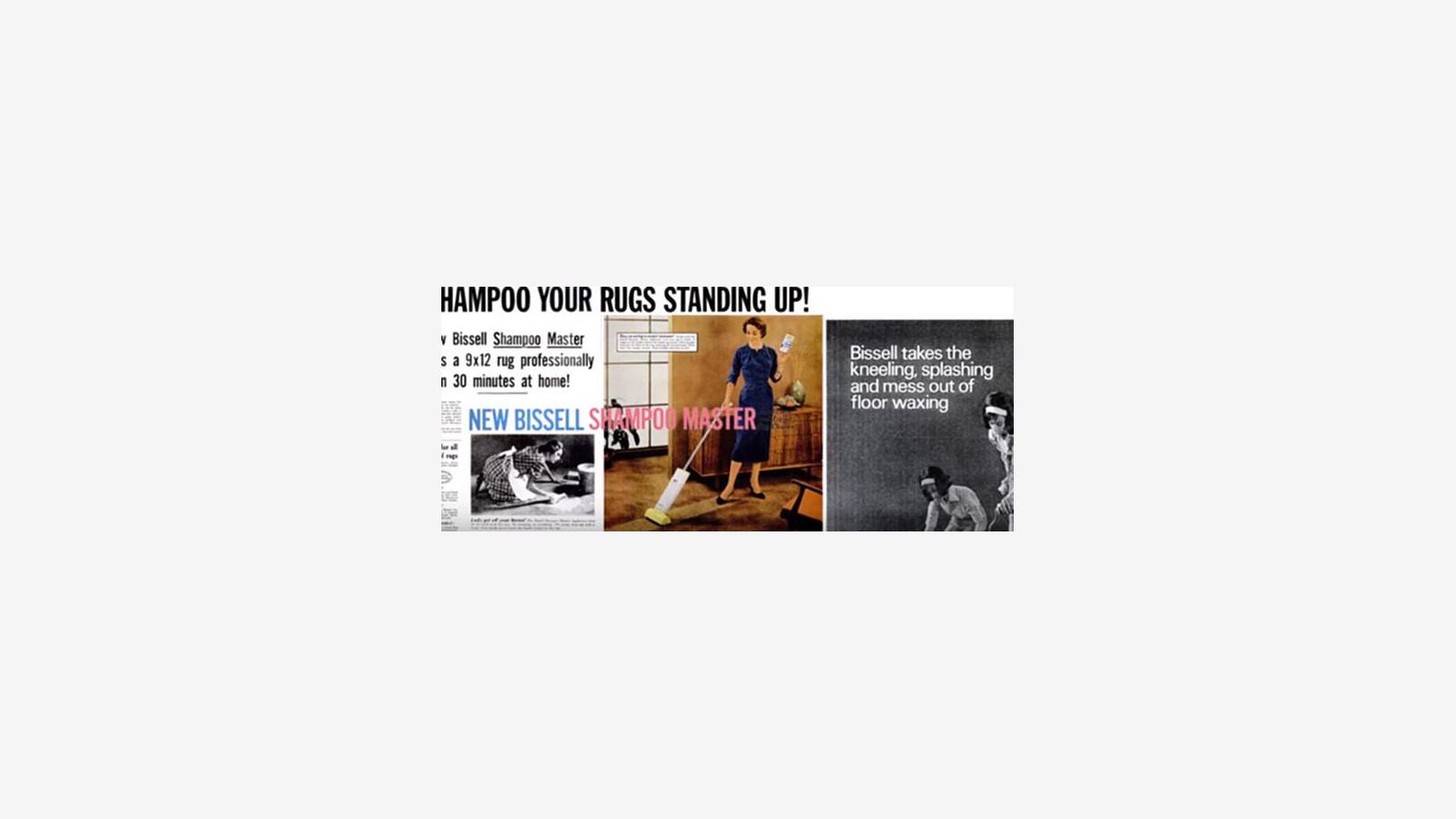

The vacuum cleaner became one of the first cleaning products to create global brands. Hoover became almost synonymous with vacuuming in some markets. Electrolux built a broad European appliance group. Miele and Vorwerk established premium and direct-selling positions. Bissell developed around floor and carpet cleaning. These companies did not only sell machines. They shaped how consumers understood home cleaning.

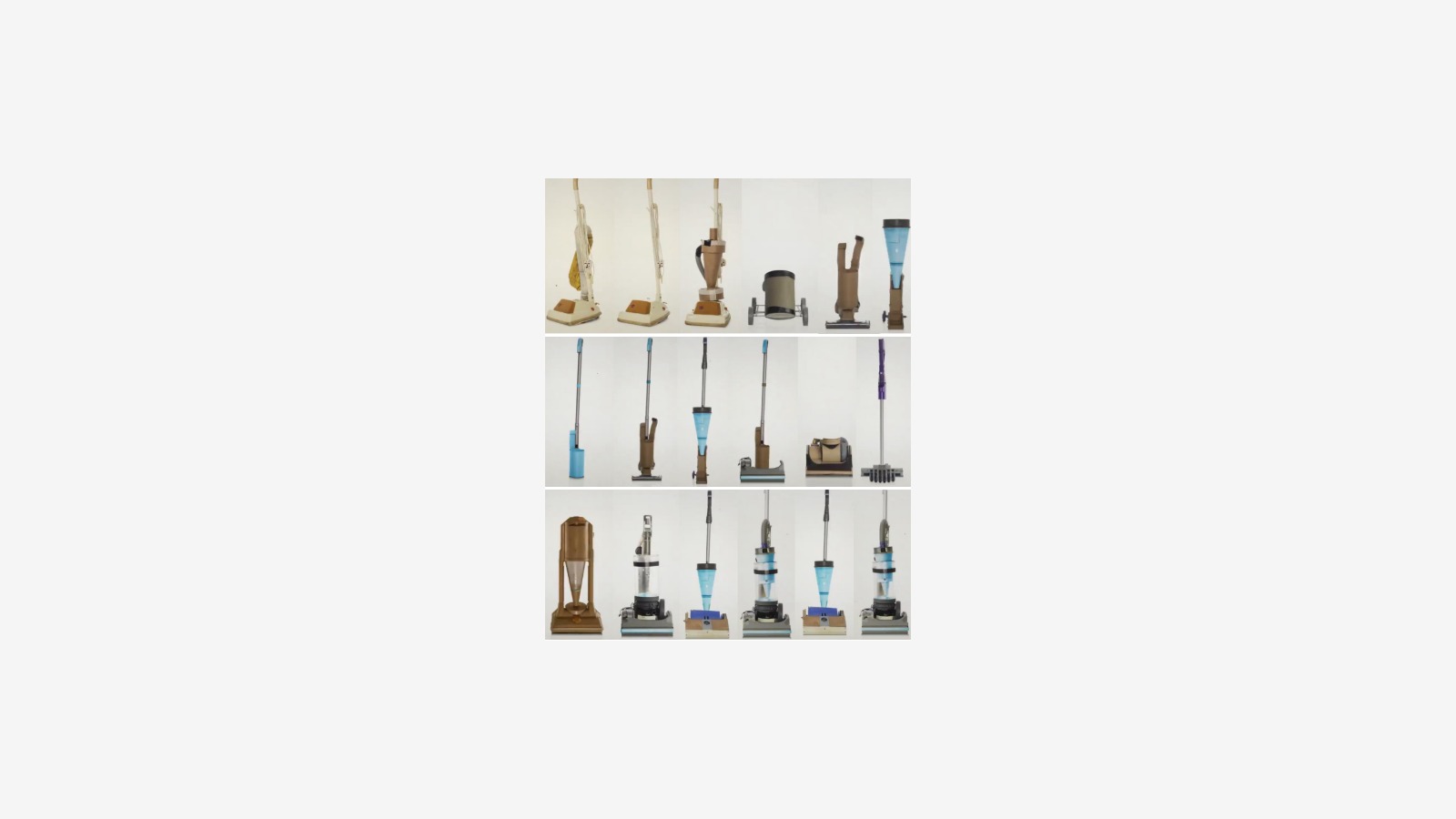

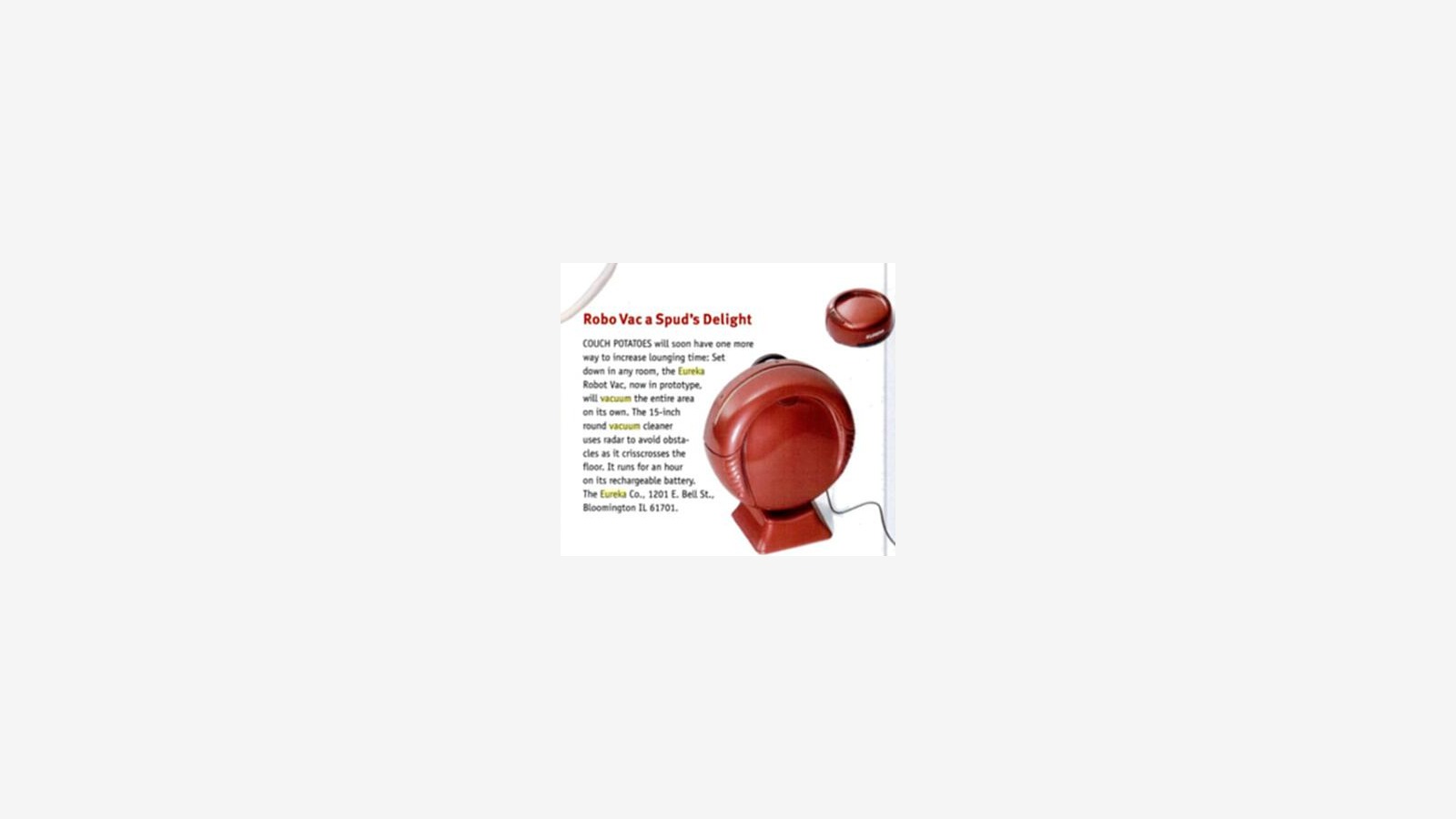

The next wave came from product format changes. Bagless vacuums challenged the traditional consumables model. Cordless handheld products changed convenience. Wet and dry cleaning created new usage scenarios. Robot vacuums later changed the relationship between user and machine: cleaning was no longer only a manual action, but an automated service inside the home.

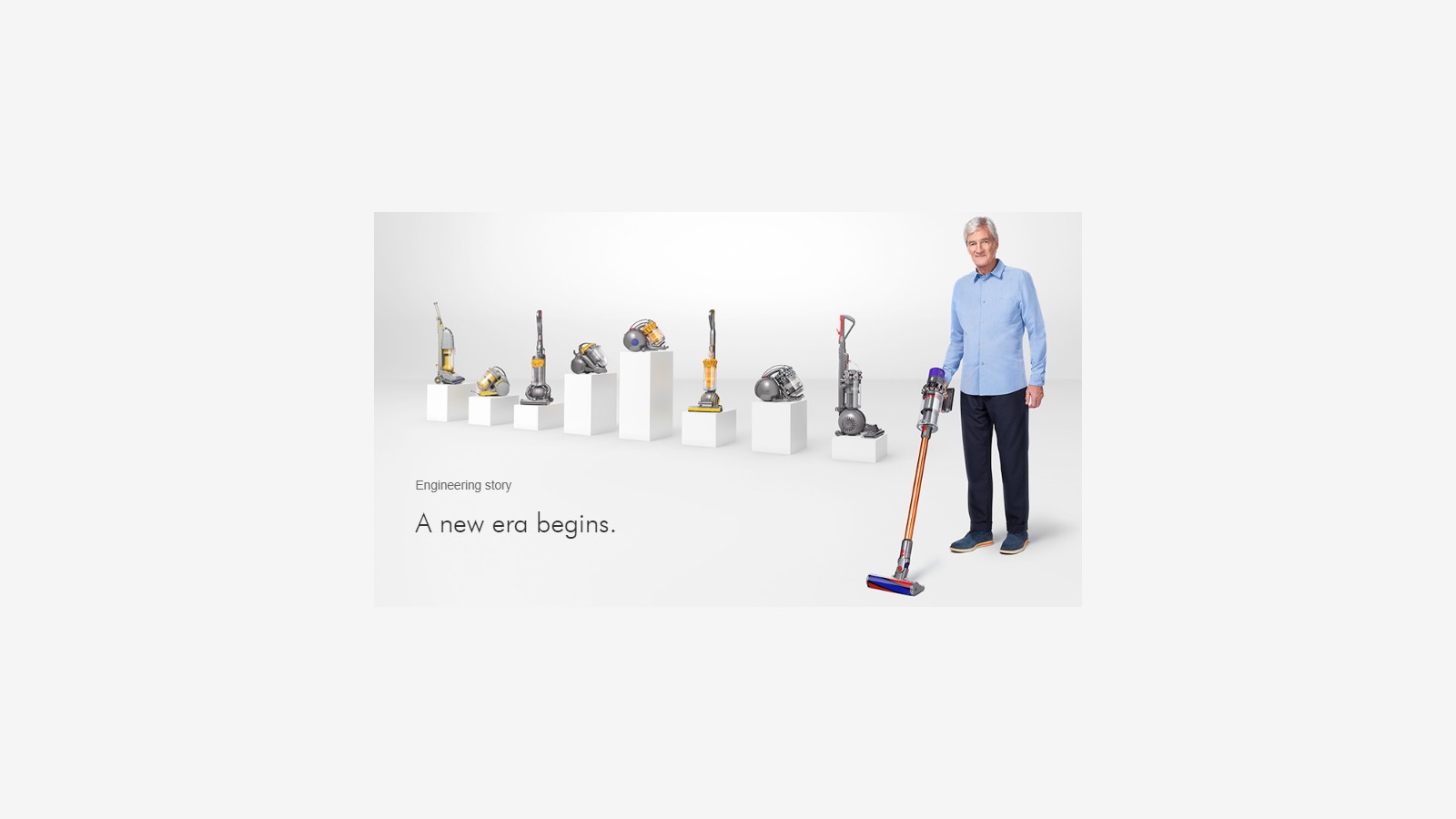

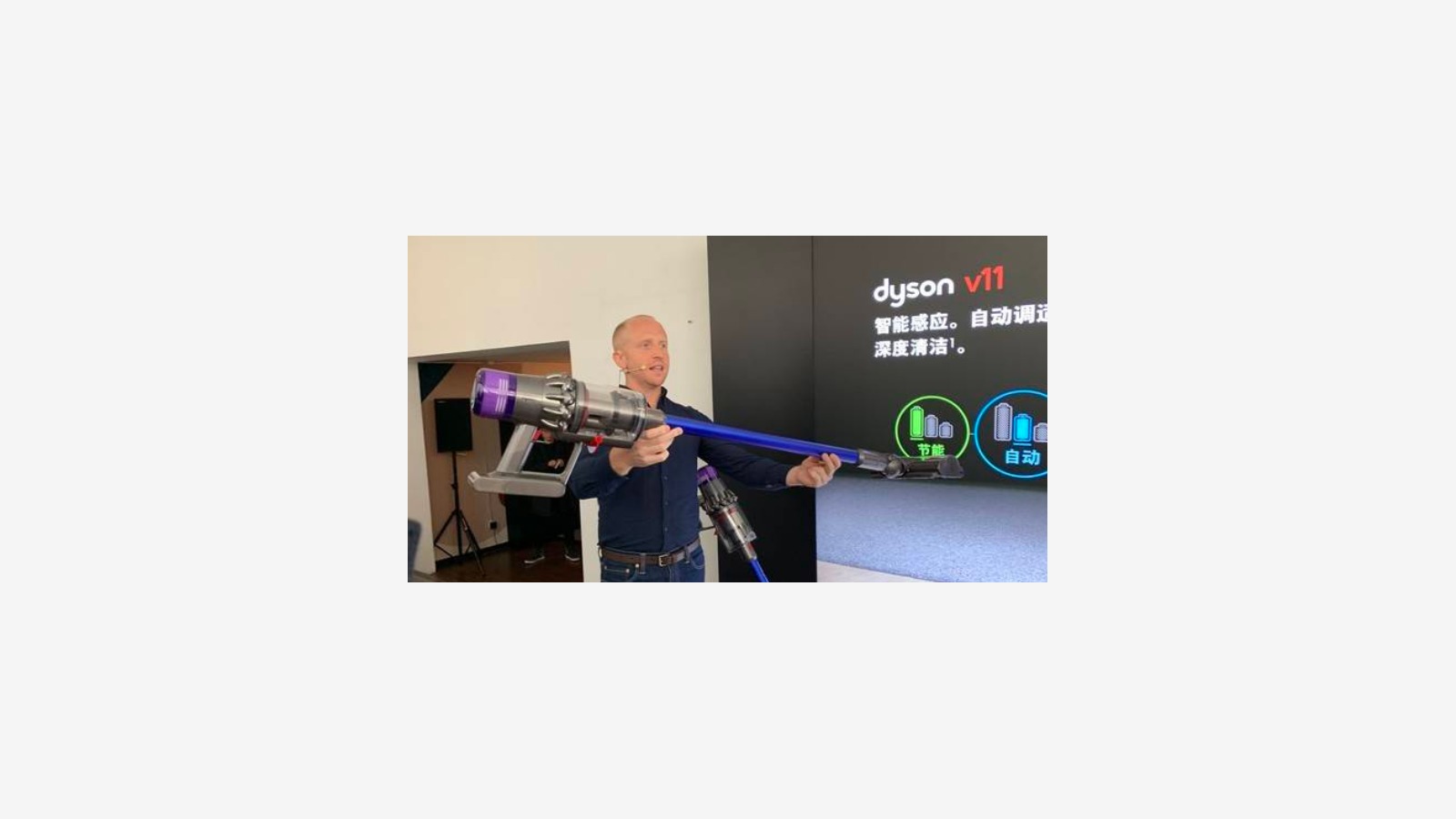

Dyson, iRobot and the Shift to Technology-Led Cleaning

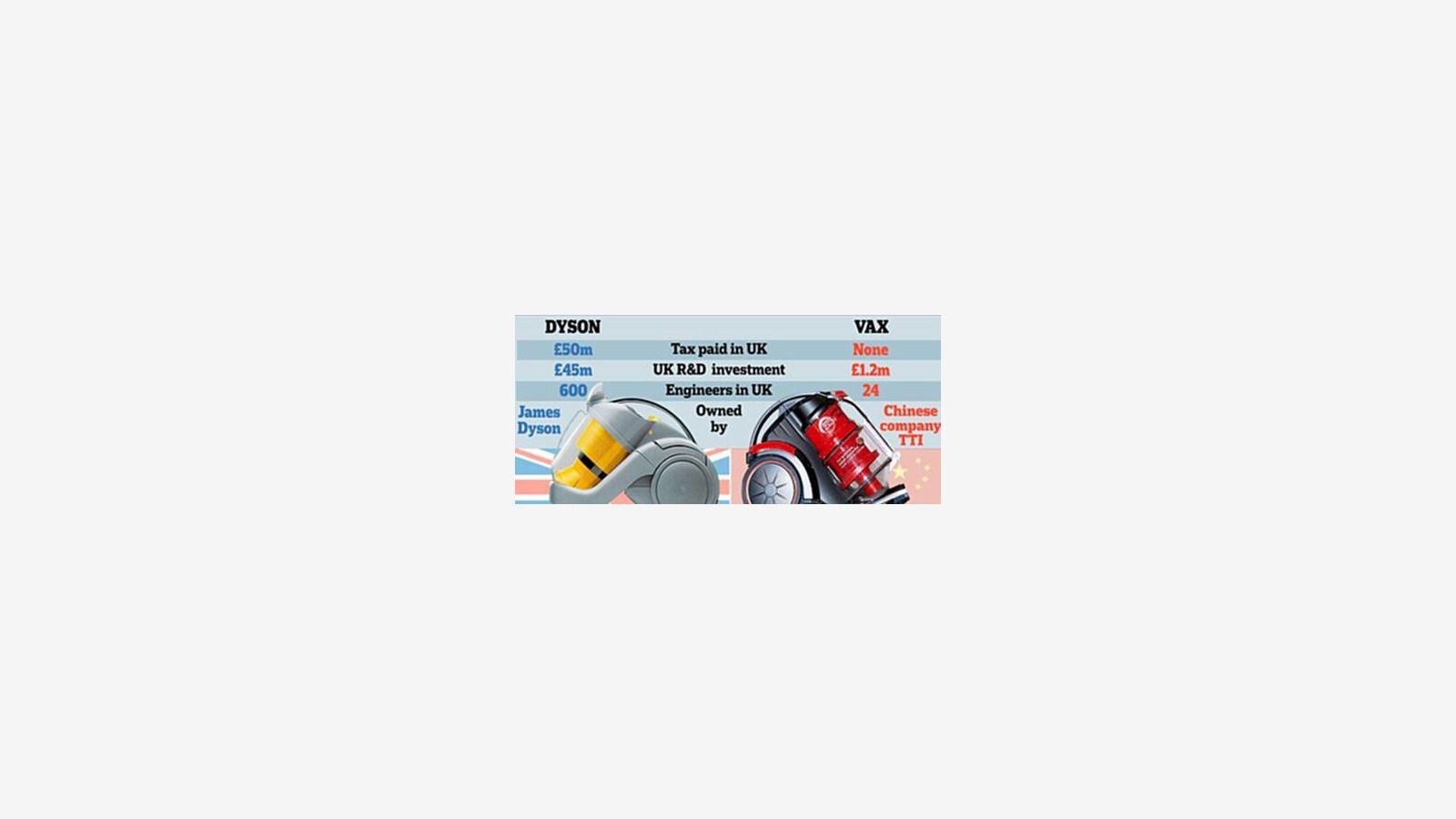

Dyson and iRobot were two of the most important symbols of the technology-led stage. Dyson changed the premium vacuum cleaner market through cyclone technology, high-speed motors and industrial design. iRobot introduced the idea that a cleaning appliance could behave like a robot, not just a motorized tool.

But the rise of these companies also showed a pattern that still matters today. A company can create a category and still face pressure when the market shifts from invention to industrial competition. Once product architecture becomes clearer, supply chain speed, cost control, channel execution and software iteration become just as important as the original idea.

China Enters the Main Stage

China’s role in the industry first came through manufacturing. Over time, it moved from OEM and ODM production to full brand competition. Roborock, Ecovacs, Dreame, Tineco, Narwal and many other Chinese companies changed the global cleaning appliance market because they combined engineering, supply chain speed, price competitiveness and rapid product iteration.

This is the real meaning of the industry’s recent shift. Cleaning appliances are no longer dominated only by old European and American brands. The new competition is increasingly defined by Chinese product cycles, robotics capability, docking stations, hard floor washers, wet cleaning systems and global e-commerce channels.

The Next Century

The next century of cleaning appliances will not be decided by suction power alone. It will be decided by automation, water management, battery systems, sensors, AI recognition, after-sales service and global supply chain organization.

For industry readers, the historical lesson is clear: every major winner emerged when it caught a change in product format. The companies that treat cleaning as a static appliance category will fall behind. The companies that understand cleaning as a changing combination of hardware, software, service and household behavior will define the next stage.